The tender offer tax trap: a Huntress case study

8 min

Yes, you'll owe AMT. That's the cost of entry for Path B. But keep reading.

0 result

Yes, you'll owe AMT. That's the cost of entry for Path B. But keep reading.

San Francisco native (yes, really). @uw and Lowell High alum. I like to nerd out on fintech, stock options and taxes.

Congrats to all Huntress employees 🎉

If you work at Huntress, you're in an enviable spot. The company has grown to over $100M in ARR, raised $338M, and is widely considered one of the most promising pre-IPO cybersecurity companies in the market. A major liquidity event like an acquisition or IPO feels closer than ever.

And if a tender or secondary offer lands in your inbox, the temptation will be hard to resist. Cash money liquidity. No waiting for an IPO. No lock-up period. Just sell and move on.

But how you sell matters enormously. And most employees default to the easiest path, selling your unexercised options, without realizing it's also the most expensive one.

The IPO window has been mostly closed for the past few years. In its place, we have found, tender offers (company sponsored sales) and secondary sales (direct to investor) have become the primary way employees at high-growth private companies like Huntress get liquidity. Companies like Stripe, Plaid, and Databricks have all offered company sponsored tender offers lately. Based on our experience, they're good for employees, and they're good for companies looking to retain talent without going public.

But selling your shares always comes with the same big tax question that IPOs always did: when do you exercise your stock options, and how?

Like the IPO situation, most employees don't think about this until the opportunity to sell is already happening. By then, for many, it's too late to do anything but take the hit.

Let's say you joined Huntress in 2021 and have 100,000 Incentive Stock Options (ISOs) with a strike price of $1.50. Huntress's last known valuation was $1.55B in mid-2024 which comes out to a $10.44 per share price, and let's assume a hypothetical tender or secondary offer values shares at $20 each today.

You have two choices:

Path A - Cashless exercise in the current tender. You exercise and sell simultaneously. Typically no cash required upfront. The full difference between your $1.50 strike and the $20 tender price — $18.50 per share is taxed as ordinary income. Simple, clean, expensive.

Path B - Exercise now, hold 12+ months, sell in the next tender. You pay to exercise today at the current 409A of $10.50, hold the shares for at least a year, and sell in a future tender or secondary. The gain from exercise to sale gets taxed at long-term capital gains rates instead. More complex. Much higher reward.

Note: All figures are illustrative. Assumptions: CA resident, married filing jointly, $200K base salary, 100,000 ISOs at $1.50 strike price, current 409A of $10.50, hypothetical tender offer at $20/share today. Actual results may vary and there is no guarantee of any particular outcome.

| Item | Value |

|---|---|

Shares sold | 100,000 |

Tender/secondary price | $20 |

Strike price | $1.50 |

Spread per share | $18.50 |

Total spread (ordinary income) | $1,850,000 |

Taxes (~53% combined Federal + CA) | ~$980,500 |

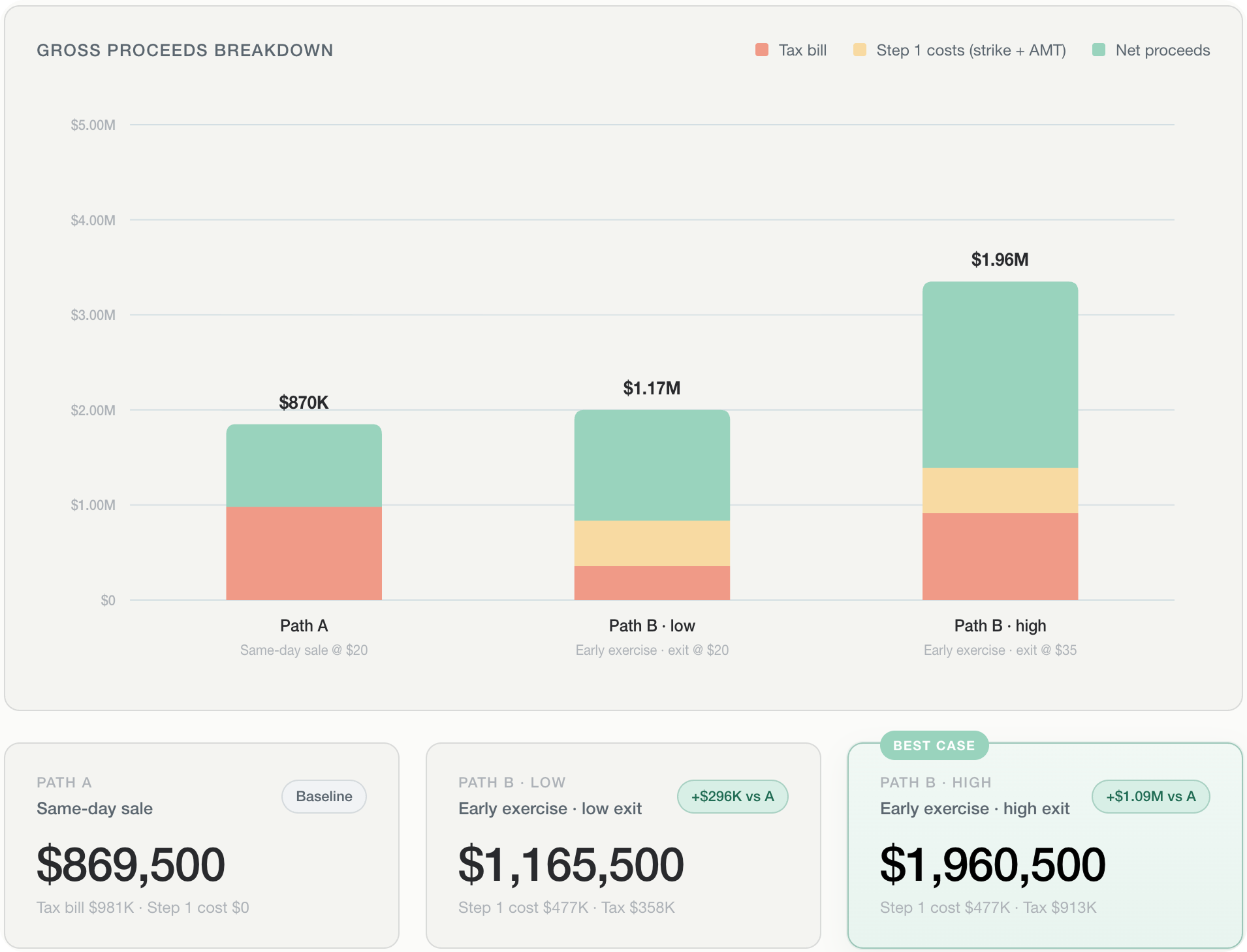

Net proceeds | ~$869,500 |

You walk away with just under $870k. That’s a great win as most companies get to an exit. But let’s run the numbers if you had exercised earlier.

You exercise today at the current 409A of $10.50.

Step 1: Exercise today

| Item | Value |

|---|---|

Exercise cost (strike × shares) | $150,000 |

Spread on exercise ($10.50 FMV - $1.50 strike) | $9/share |

Total ISO spread | $900,000 |

Estimated AMT on exercise | ~$327,000 |

Step 2: Sell in next tender at $20/share (12+ months later)

| Item | Value |

|---|---|

Sale price | $20 |

Strike price (your cost basis) | $1.50 |

Long-term capital gain per share | $18.50 |

Total long-term capital gain | $1,850,000 |

Taxes (~37% combined federal LTCG + NIIT + CA)* | ~$684,500 |

AMT credit recovered from Step 1 | ~($327,000) |

Estimated total tax (Step 2) | ~$357,500 |

Gross proceeds from sale | ~$1,642,500 |

Less: Step 1 out of pocket ($150K strike + $327K AMT) | ~($477,000) |

Potential Net proceeds | ~$1,165,500 |

* 37% reflects the 20% federal LTCG rate + 3.8% net investment income tax (NIIT) + 13.3% CA state rate.

That's the pure tax savings between Path A and Path B with the same $20 exit price, accounting for every dollar spent along the way. By exercising at least a year prior to selling, you could get to keep an extra $295K without the stock moving a single dollar.

The $20 comparison isolates the tax savings. But Path B has another potential advantage the cashless exercise never will: you still own the shares. If Huntress grows and the shares are now worth $35, the numbers get dramatically more compelling.

Step 2 (revised): Sell at $35/share (12+ months later)

| Item | Value |

|---|---|

Sale price | $35 |

Strike price (your cost basis) | $1.50 |

Long-term capital gain per share | $33.50 |

Total long-term capital gain | $3,350,000 |

Taxes (~37% combined federal LTCG + NIIT + CA) | ~$1,239,500 |

AMT credit recovered from Step 1 | ~($327,000) |

Estimated total tax (Step 2) | ~$912,500 |

Gross proceeds from sale | ~$2,437,500 |

Less: Step 1 out of pocket ($150K strike + $327K AMT) | ~($477,000) |

Net proceeds | ~$1,960,500 |

Compared to Path A's ~$869,500, Path B at $35 may leave you with roughly $1.09M more — that's the combined effect of lower tax rates and price appreciation working together.

| Item | Path A | Path B ($20) | Path B ($35) |

|---|---|---|---|

Exit price | $20 | $20 | $35 |

Net proceeds | ~$869,500 | ~$1,165,500 | ~$1,960,500 |

You keep vs. Path A | — | +$296,000 | +$1,091,000 |

For illustrative purposes only. Actual results may vary and there is no guarantee of any particular outcome.

This is an honest question, and it deserves a straight answer.

Path B requires two things to go right: (1) there’s active buyers in Huntress stock, or the company goes public, and (2) the share price holds or appreciates. Neither is guaranteed. Huntress has mentioned that they have IPO ambitions, and companies at this stage of growth may often run multiple tenders before going public, but "often" is not "always."

This is a planning decision, not a prediction. If you're confident in Huntress's trajectory and can afford to part with the exercise cash (or finance it), the tax math is compelling. If the exercise cost would cause you real financial stress, or if you need liquidity now, Path A is still a perfectly reasonable choice.

The point isn't that one path is always right. It's that you should make the choice consciously, not just click the default.

Here's the thing about liquidity events: they feel like a gift. And they are given how rare liquidity events are in the startup world. But the way most employees respond in a reactive, not a proactive planning way is the financial equivalent of leaving a briefcase full of cash on the table because picking it up felt like too much work.

The numbers in this case study aren't hypothetical edge cases. They're what the math looks like for a real employee at a real company, using conservative assumptions. A $296K difference just from smarter tax planning. A $1.09M difference if the company keeps growing. These aren't rounding errors

I've had this conversation hundreds of times. Every IPO, every tender offer, the story repeats itself. Employees who planned ahead walk away with dramatically more. Employees who defaulted to selling unexercised options, did the math afterwards, and were surprised to see their take-home cut in half.

Start thinking about it now. Run your numbers. Understand what each path actually means for your specific situation. And if you're not sure where to start, talk to someone who does this every day.

If you're a Huntress employee exploring selling your shares, we can help.

1. Planning — know your numbers before you decide. Our equity strategists work with employees at companies like Huntress every day. We'll walk through your specific situation including your strike price, vesting schedule, tax profile, and liquidity needs, and help you understand exactly what each path costs you. No pressure, no commitment.

2. Financing — cover the exercise cost if cash is the obstacle. The biggest barrier to Path B is often the upfront cost. In this scenario, that's $477K out of pocket before you see a single dollar of proceeds. Secfi's non-recourse financing provides cash against your equity to cover the exercise cost and AMT, so you can pursue the tax-efficient path without draining your bank account or risking your home. You repay when you sell your shares or after the exit and the hope is a win-win scenario where you take home more after exit.

The AMT calculation in Path B is real and worth understanding before you exercise. When you exercise ISOs, the spread between your strike price and the fair market value becomes an AMT preference item. Depending on your income and the size of the spread, this can mean a real tax bill in the year you exercise — even though you haven't sold anything yet.

The good news: AMT paid at exercise becomes a credit you can use to offset your regular taxes in future years. So it's not money lost forever. But you do need the cash to cover it in year one.

Use our AMT Calculator to see exactly what you'd owe before you decide.

Disclaimer: All figures used in this article are illustrative and based on hypothetical assumptions. There is no guarantee of any particular result. This is not tax or financial advice. Individual results will vary based on your specific situation, tax profile, and company outcomes. Please consult a tax professional regarding your particular circumstance. Huntress has not announced a tender offer. Past performance is not indicative of future results.