📍 State of the Private Markets Q1 2026

0 result

San Francisco native (yes, really). @uw and Lowell High alum. I like to nerd out on fintech, stock options and taxes.

Hey there,

Vieje back again. It’s been a hectic week as I just moved to another apartment in Brooklyn. Despite quite literally being a block and a half away, the cost of movers is over $1,200 for a 2-bedroom apartment. The last time I paid movers in New York was 10 years ago in 2016, and we paid $600 plus tip for a 2-bedroom move. Lots has changed in those 10 years and it hasn’t gotten cheaper to live in New York.

On the topic of change, I wanted to write today’s newsletter about the state of the private markets. Our friends at Caplight provided some great data in their Q1’26 Secondary Market Update, and I’ll bring in some slides from that deck to help guide the narrative.

Let's get into it.

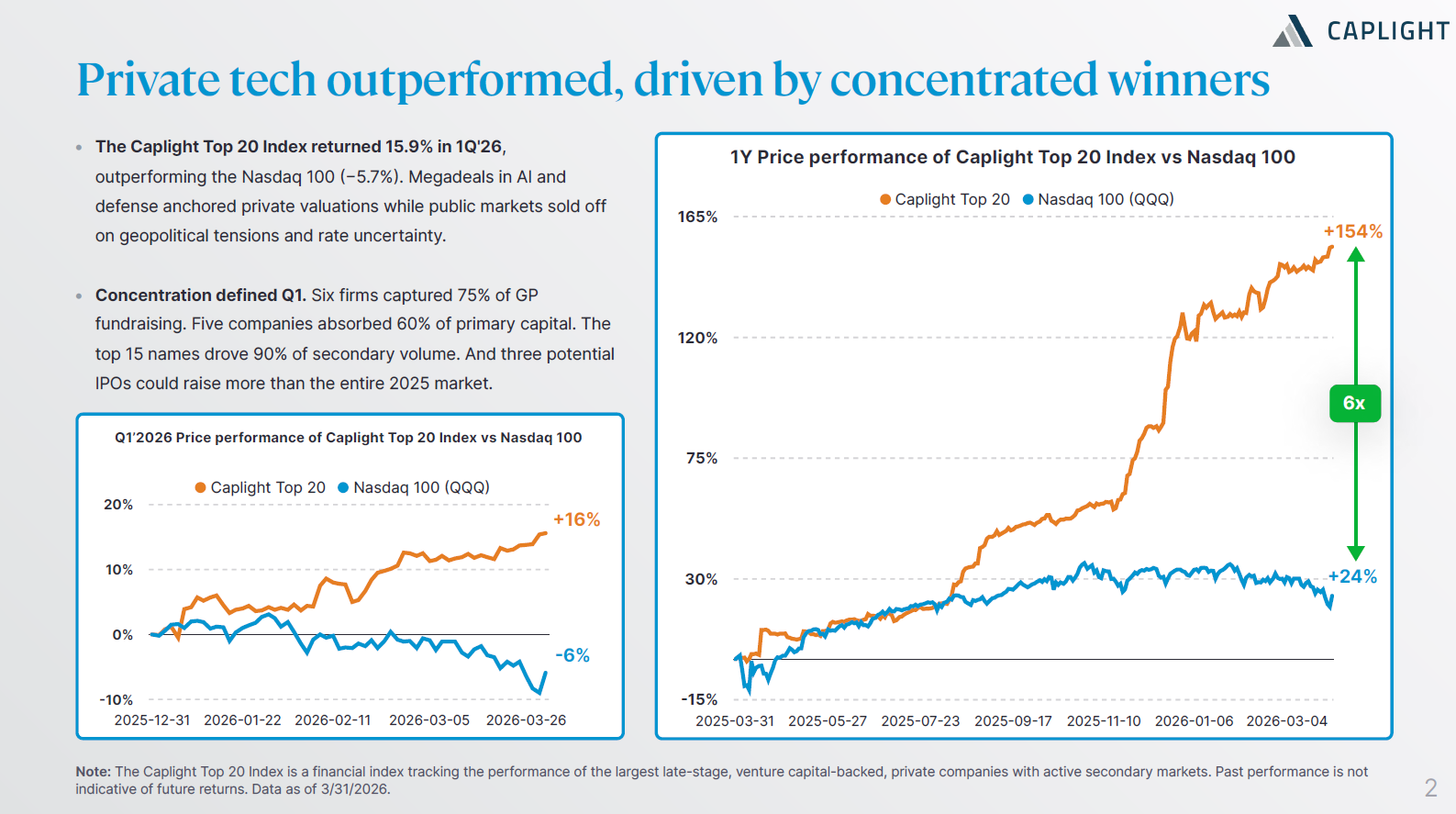

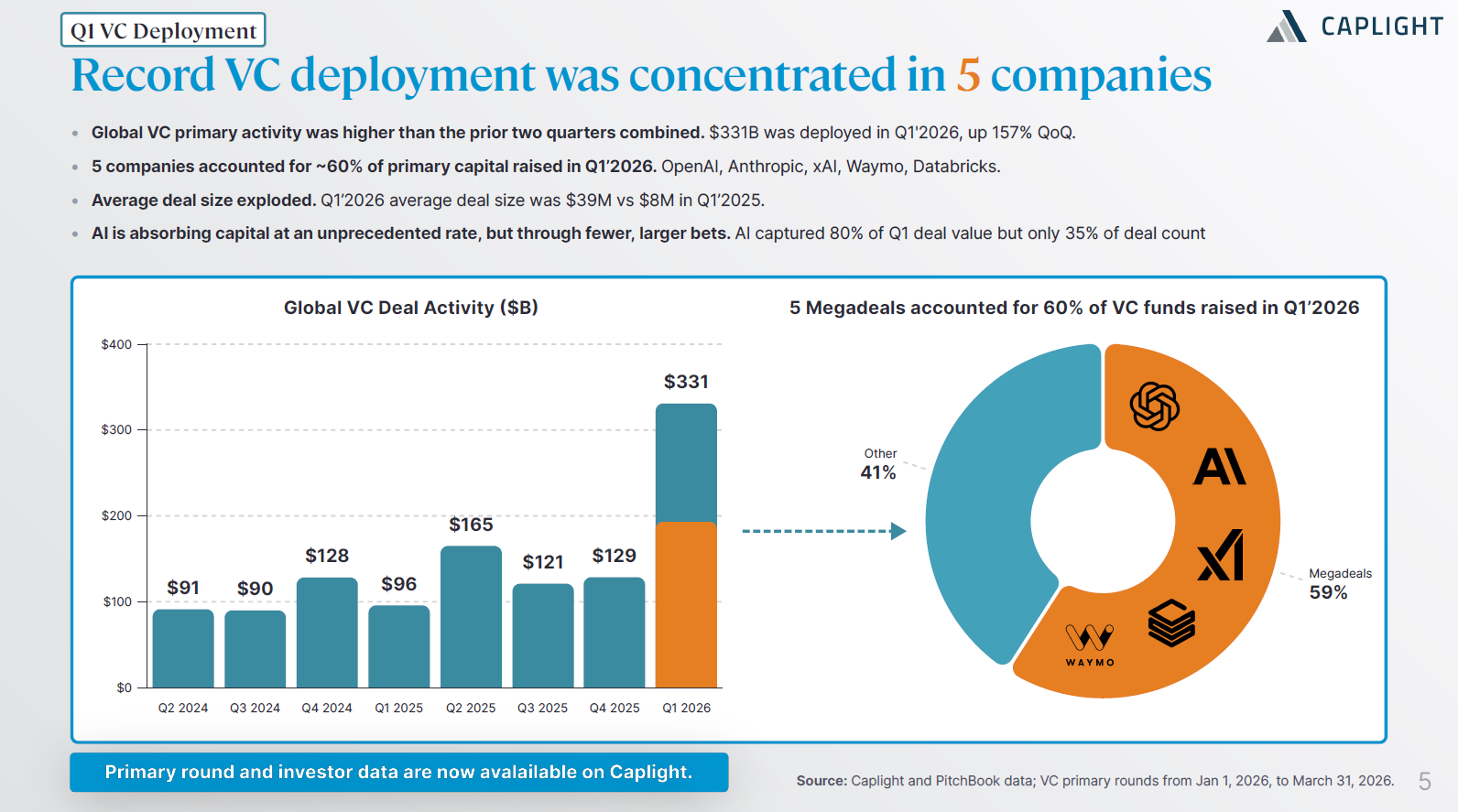

If you think you’ve heard me say this before, you’re not going crazy. There is a large concentration building among mega-cap companies in the private markets. The majority of direct and secondary investments are going into the top handful of companies. This has been the theme of the last few years after the ZIRP years ended and the market reset.

This has been a growing trend and given the capital expenditures of AI companies, I don’t see things slowing down anytime soon. There is an unprecedented level of demand for access to certain companies. We’ve spoken about this before as more firms are looking to “provide access” to the private markets.

For those at these top companies, liquidity is abundant which has been the case for the last few years.

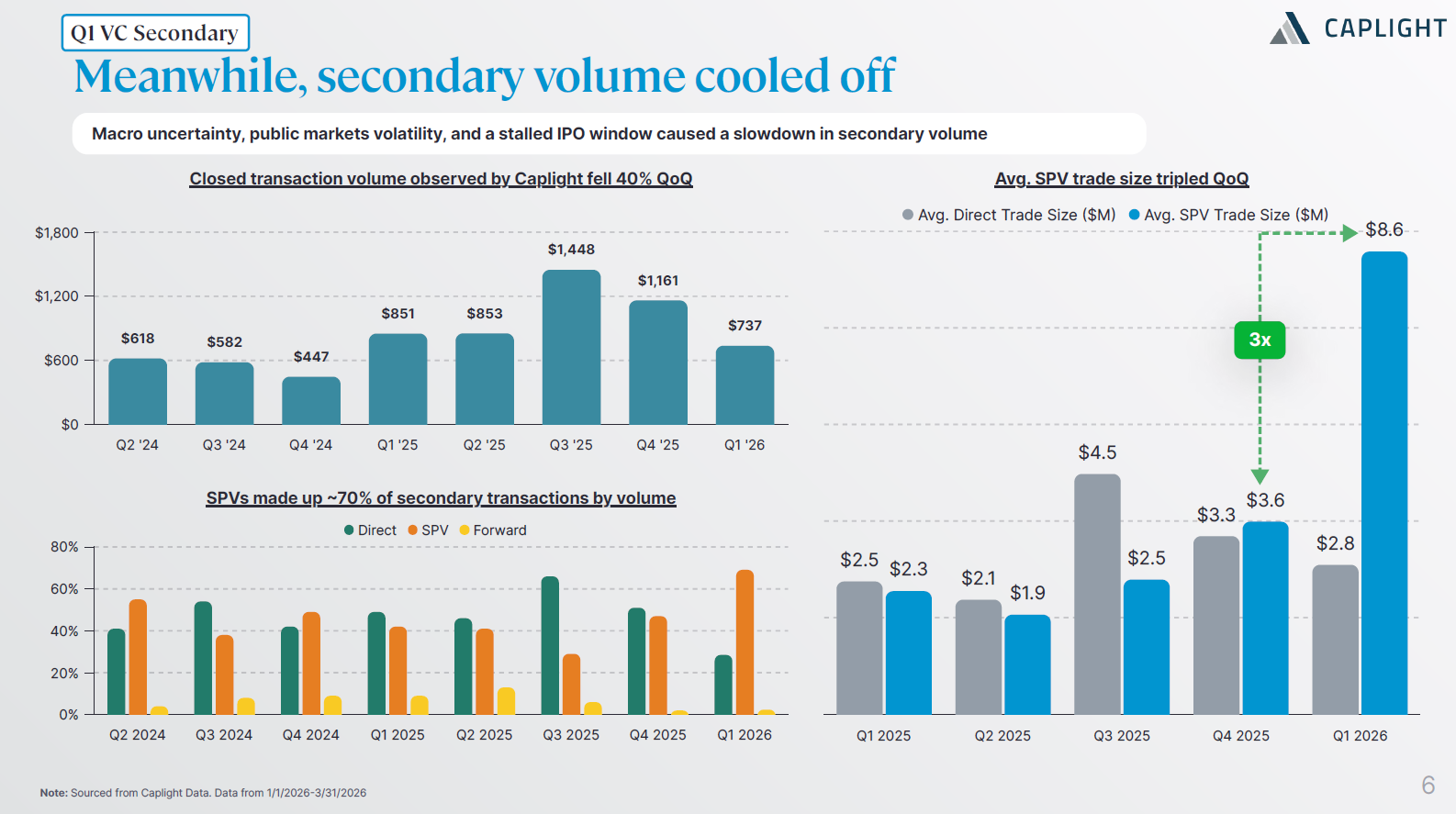

For folks looking for liquidity at companies outside of the top companies in the AI, defense, and data space, things are looking a lot more difficult which again has been thematic of the post ZIRP years.

There was a short lived resurgence in 2025 for the secondary markets, peaking in Q3 2025 on the back of a hopeful IPO window for tech companies. We saw a handful of companies such as Netskope, Figure, and Via hit the public markets in the second half of 2025. Unfortunately, the secondary markets have been on a steady decline since then as the public markets have not been kind to new tech entrants.

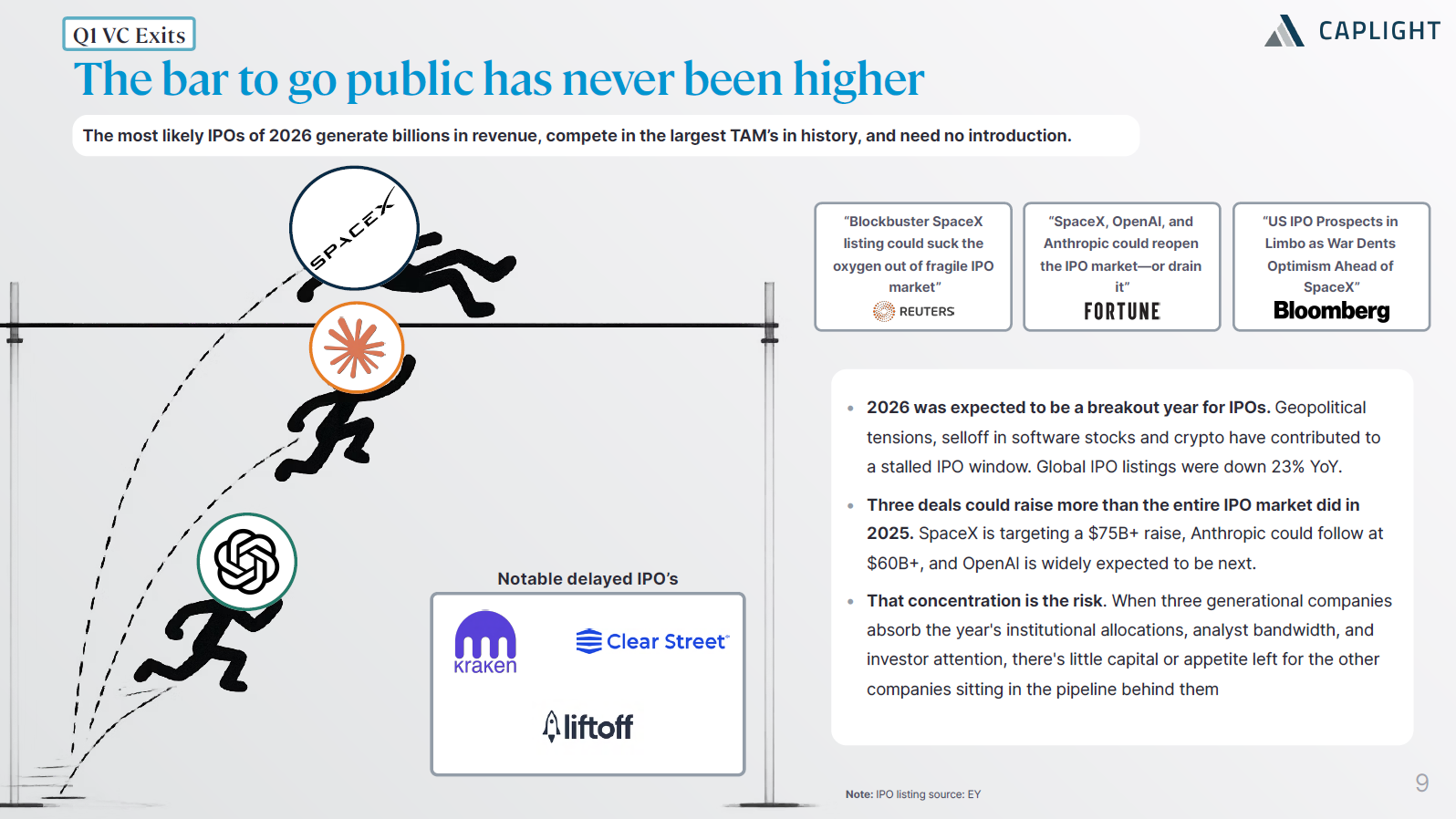

Yes and no. The most anticipated IPO of the year (decade?) is coming next month with SpaceX expecting to finally go public after filing a confidential S1 earlier this year. There have been rumors of OpenAI and Anthropic also looking to enter the public markets. The theme of this year’s IPO window is the mega-IPO. That is perhaps 3 companies looking to go public with a market cap of over $1T.

So what about the rest of the companies? The path to the public markets is likely going to be very challenging this year for anyone outside of those 3 companies. With the attention and capital focused on SpaceX, and then potentially OpenAI and Anthropic, the word on the street is that most companies are likely going to wait for the dust to settle first before potentially being overshadowed.

There’s a lot of frustration among a lot of employees at pre-IPO companies right now. With the secondary market in an overall decline and a closed IPO window for the majority of companies, liquidity has been difficult to come by.

The optimistic view is that if these IPOs go well, we could see other companies start to test the waters by filing S1s in the second half of the year. For now, the majority of the pre-IPO world is in wait and see mode.

Let us know what you think by replying below. Until next time!