83(b) election for stock options: when it makes sense to file

2 min

0 result

Mike’s a CPF® at Secfi. He specializes in helping clients make the most of their stock options and integrate equity compensation into their broader financial plans.

If your company lets you exercise stock options early, you may have a short window to make a decision that can have a big impact on how much tax you pay. That’s where an 83(b) election for stock options becomes something you need to consider.

The 83(b) election lets you choose to be taxed when you exercise early, instead of waiting for later when you earn the shares of stock over time (vesting).

The tricky part is that most startup employees only hear about 83(b) election stock options when they’re already in the middle of exercising, staring at tax or grants forms, and realizing there’s a 30-day IRS deadline.

And the stakes can feel high, because a single decision now can affect your taxes, risk exposure, and potential upside for years to come:

But we’ve got you covered. In this guide, you’ll find:

Note: Secfi provides equity planning guidance, tools and financing so startup employees can own their stock options with confidence. If you’re looking to better understand what you can do with your equity, sign up to our free platform here: Get Started.

The name refers to a provision under section 83(b) of the Internal Revenue Code (IRC) that allows a taxpayer to choose between being taxed on equity compensation today versus when it vests. This election is most typically used because the strike price is equal to the 409A, which means there is little tax when they early tax.

By filing a section 83(b) election, you can pay tax on the 409A valuation of company shares today versus their 409A valuation in the future, which may be higher. The 409A valuation (also known as fair market value or FMV) is reevaluated every 12 months and grows as your company becomes more successful.

This timing difference can potentially result in significant tax savings if your company increases in value, as more of your gains will be federally taxed at capital gains tax rates (typically 15-20%) rather than ordinary income tax rates (up to 37%). For many tech employees, that gap is the difference between a manageable tax bill and a painful one.

A quick note: the 83(b) election does not apply to restricted stock units (RSUs). RSUs follow a different set of tax consequences because they aren't considered property under section 83 at the grant date.

Tax treatment comparison:

For illustrative purposes only. Actual results may vary and there is no guarantee of any particular outcome.

| Without 83(b) election | With 83(b) election |

|---|---|

- No ordinary income tax at early exercise for the unvested shares - Taxed as ordinary income when shares vest (based on FMV at vesting) - Capital gains holding period starts at vesting | - Taxed as ordinary income at exercise (based on FMV at exercise) - No additional tax when shares vest - Capital gains holding period starts at exercise

|

Early exercising is when you exercise your stock options before they vest. This is usually when an 83(b) election becomes relevant, because you’re buying shares that you don’t fully own yet. People usually consider early exercise because it may let them buy shares when the company’s value is still low, potentially reducing their taxes if the company becomes more valuable later.

When your company is still early-stage, the difference between your strike price and the fair market value may be minimal, meaning little or no tax is due at exercise. That makes it less expensive to exercise and helps limit your risk if the company doesn't succeed or have a successful exit.

But it’s not always possible to exercise early, as companies have to specifically allow it. Ask your employer or check your option grant if you're not sure whether this is the case for you.

If your employer allows you to early exercise stock options, there may be significant tax savings, especially if your strike price and the company's fair market value valuation are relatively close.

Early exercise may provide:

For Non-Qualified Stock Options (NSOs), long-term capital gains tax treatment applies if you hold the shares for at least one year after exercising.

Incentive Stock Options (ISOs) are more nuanced. If you early exercise ISOs, they may no longer qualify for ISO tax treatment and may instead be taxed like NSOs. An 83(b) election can still help you lock in the current fair market value for tax purposes, but it’s worth talking to a tax professional before filing.

For a full breakdown of when to exercise your options, read our guide: When should you exercise your stock options?

Now that we’ve covered the basics, it’s time to figure out what to actually do with an 83(b) election for stock options. That means evaluating if exercising early is the right choice for your current situation.

The decision depends on several factors:

You’ll also may want to consider taxes. In particular:

There are risks to consider if you want to exercise your stock options earlier:

There are two ways to file an 83(b) election for stock options:

Option 1: New IRS Form 15620 (recommended for 2026). The IRS introduced Form 15620 in 2024, providing a standardized form for 83(b) elections. This reduces filing errors and is now the preferred method.

Option 2: Written statement (traditional method). Download and complete the 83(b) election form and cover letter. Your company may provide templates, or platforms like Carta or Shareworks can generate them.

83(b) election for stock option filing requirements:

Critical deadline: This must be completed within 30 days of your early exercise. No exceptions. A late filing can eliminate the tax benefits and expose you to a larger tax bill in the future.

At Secfi, we help startup executives and employees make these types of decisions every day. If you’re trying to decide whether early exercise makes sense for you, you don’t have to figure it out from IRS forms, spreadsheets, and Reddit threads.

Here’s why employees at companies like Databricks, Anduril, and Canva work with Secfi:

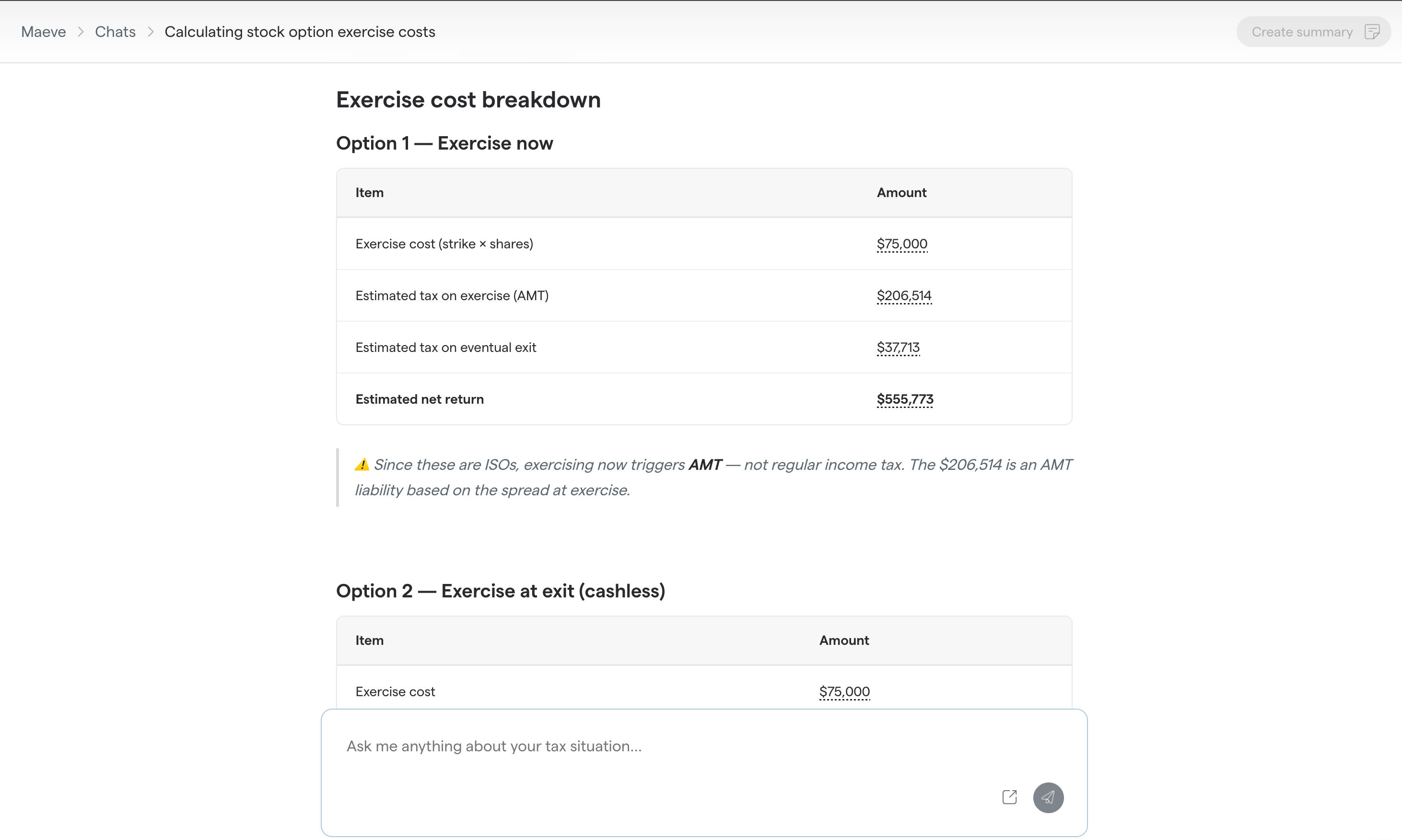

Before you early exercise or file an 83(b) election, it helps to understand what your options could cost, how taxes may change across different scenarios, and what you might gain or lose if your company exits.

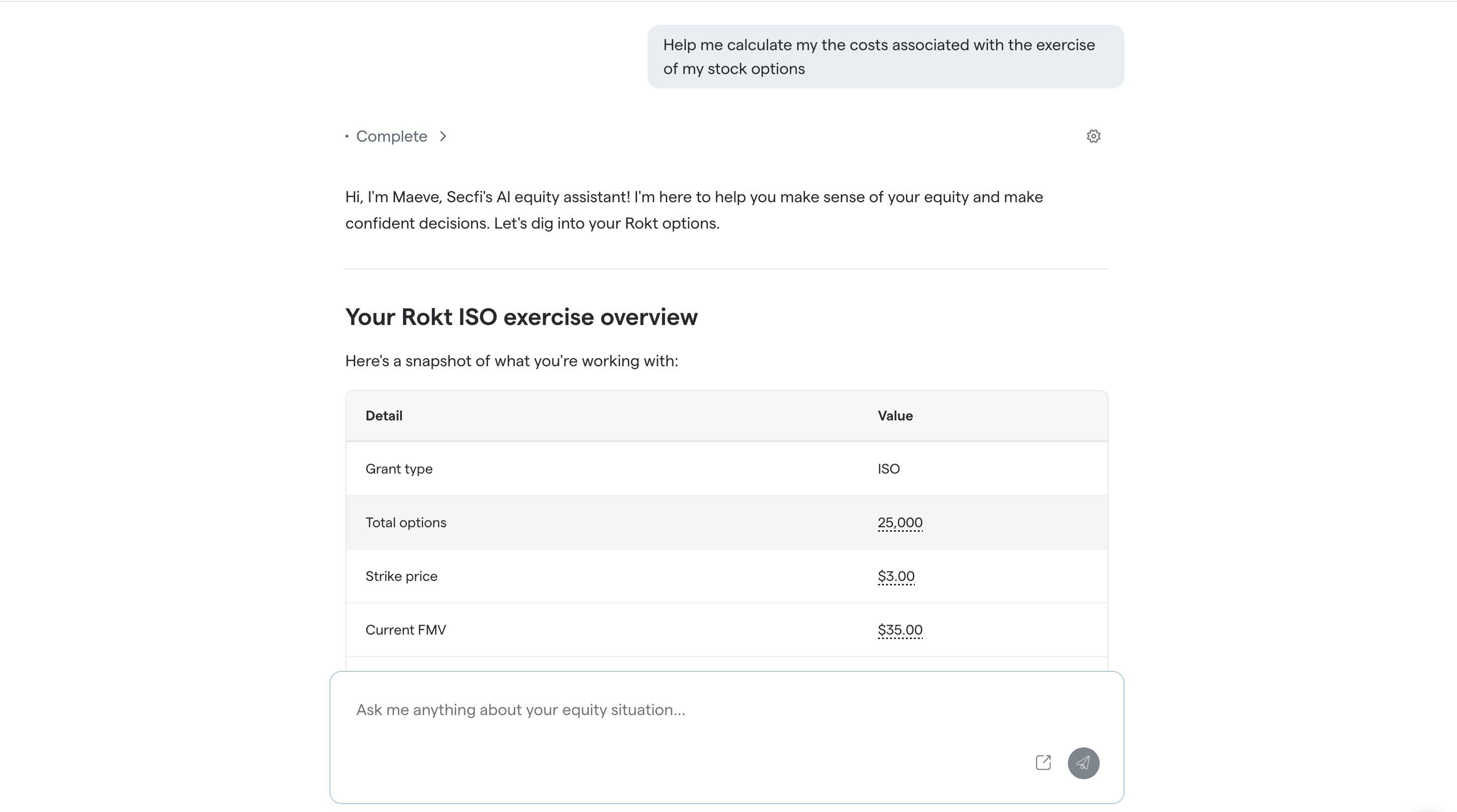

Maeve, Secfi’s AI equity planner, was built to help you get clearer answers about your stock options, exercise timing, taxes, and potential outcomes. You can use it to ask questions about your equity, and start making sense of your next steps before you commit cash to exercising.

You can get started with Maeve by signing up for free here: Get Started. You can then upload your grant information or connect to Carta in just a few seconds, so your actual data can be used right away to give you personalized scenario modeling.

For illustrative purposes only. Actual results may vary and there is no guarantee of any particular outcome.

Work with Secfi’s equity specialists if your situation is more complex

An 83(b) election can be a high-stakes decision because the right move depends on your grant details, company stage, strike price, 409A valuation, tax situation, and how long you expect to stay.

Secfi’s licensed equity and wealth specialists can help you walk through those details, compare different exercise scenarios, and understand how early exercise fits into your broader financial plan.

If you don’t want to use your own cash or take out a personal loan to exercise your stock options, non-recourse financing is worth considering.

With non-recourse financing, Secfi covers the cost to exercise your options and, depending on your situation, the taxes due at exercise. You don’t make monthly payments. Instead, you repay the financed amount plus fees if your company has a successful exit, like an IPO or acquisition.

If your company doesn’t exit, or your shares end up being worth nothing, you don’t have to repay the financing. Your personal assets are therefore not at risk.

That can make early exercise more realistic if:

Non-recourse financing can be a helpful option for startup employees who want to exercise their stock options without using personal savings or taking on traditional debt. In exchange for providing the upfront capital, Secfi typically shares in a portion of the future upside if your company exits successfully. For many employees, that tradeoff can make it easier to own their equity with greater flexibility and less personal financial risk.

For a full overview, check out: What is non-recourse financing for stock options?

An 83(b) election can help you reduce future taxes if you early exercise and your company grows in value. But it’s hard to make that decision before you know whether your shares will ever be worth anything.

That’s why the best next step is to model the numbers before you exercise. At Secfi, we help startup employees and executives understand their stock options, compare exercise scenarios, and fund their exercise and AMT taxes with non-recourse financing.

Try our AI equity planner Maeve to ask questions about your equity, taxes, and exercise timing.

The tool shown here uses artificial intelligence and is for illustrative purposes only and not necessarily indicative of future results and there is no guarantee that similar results can be achieved. The information provided by the tool is not professional advice and is not intended by Secfi, Inc., its affiliates, and Secfi representatives, to be deemed as investment, legal, tax or other professional advice or recommendations of any kind, or to form the basis of any decision to do or to refrain from doing anything. Secfi does not review the accuracy or completeness of the information provided to us within the tool.

If you miss the 83(b) election deadline, you generally lose the ability to make the election for that stock option exercise. The IRS deadline is 30 days from the date the property is transferred, which usually means 30 days from the date you early exercise.

That means you may be taxed later as your shares vest, based on their fair market value at the time of vesting. If your company’s valuation increases, that could lead to a higher tax bill than if you had filed the 83(b) election on time.

If you’re close to the deadline, talk to a tax professional as soon as possible. You can also use Maeve, Secfi’s AI built for equity, to better understand and model what an 83(b) election could mean for your specific situation.

Usually not. An 83(b) election must be filed with the IRS no later than 30 days after the date the property is transferred.

There generally isn’t a “late filing” option if you miss the deadline, which is why timing matters so much. If you already missed the deadline, it’s worth speaking with a tax professional to understand what happens next and how your shares may be taxed as they vest.

Secfi is focused on equity to help tech startup employees think through future exercise decisions, model tax scenarios, and avoid making the same mistake on future grants or exercises.

You may need to file an 83(b) election if you early exercise ISOs before they vest and want to be taxed at the time of exercise rather than as the shares vest.

The 83(b) election is generally relevant when you receive property that is still subject to a substantial risk of forfeiture, such as unvested shares from an early exercise. The election lets you choose to include the taxable amount in income at the time of transfer instead of later, when the shares vest.

For ISOs, there’s an extra wrinkle: exercising ISOs can also have alternative minimum tax (AMT) implications. The right move depends on your strike price, 409A valuation, income, state, and how many shares you exercise.

Maeve is, our purpose-built AI that can help you understand the basics of how ISOs, early exercise, 83(b) elections, and AMT fit together. For a more detailed decision, Secfi’s equity strategists can help you compare exercise scenarios with your actual numbers.

No. At the moment, 83(b) elections generally must still be mailed to the IRS, even though the IRS now provides Form 15620 to standardize the process.

After completing and signing the form, you should:

Many people use certified mail with a return receipt so they can prove the election was submitted on time.

Because IRS filing requirements can change, it’s still worth checking the latest IRS instructions before you file.

An 83(b) election may still be worth considering if your company might not exit, but only if you’re comfortable with the risk.

The potential benefit is that you may pay tax earlier, when your shares are worth less, and start your capital gains holding period earlier. But if your company never exits, goes down in value, or becomes impossible to sell, you may not recover the money you spent to exercise or pay taxes.

This is why the decision comes down to your numbers and your risk tolerance.

If you want to understand the tradeoffs before making a decision, try Maeve AI to ask questions about your equity, exercise timing, and taxes. You can also get in touch with Secfi’s team to walk through your situation with an equity specialist.