What is the AMT credit?

3 min

0 result

San Francisco native (yes, really). @uw and Lowell High alum. I like to nerd out on fintech, stock options and taxes.

You may be doing research on Alternative Minimum Tax (AMT) credit for a few reasons:

Whatever the case, you are likely at a stage where you’re carefully planning an exercise strategy and trying to figure out how AMT fits into your wider tax planning. AMT is one of the most complex aspects of exercising stock options and ensuring you minimize the tax requires careful planning.

In this article, we will break down:

Note: Secfi is a liquidity and wealth management service that enables employees to get the most from their stock options through our financial models, financing tools and educational support. Use our AI calculator Maeve to calculate the tax and tax credit you may owe. Please note that this is

The alternative minimum tax credit is a dollar-for-dollar reduction for any additional taxes you have paid in previous years due to the alternative minimum tax.

If you paid more income tax than you otherwise would have because of AMT, the IRS keeps track of that difference, and lets you use it to lower your tax bill in future years.

This is particularly relevant for startup employees who exercise ISOs. When you exercise ISOs and don’t sell the shares in the same calendar year, the “bargain element” (the difference between your strike price and the company’s 409A valuation, which is essentially the fair market value of your shares) can trigger AMT, even though you haven’t received any cash.

One thing to know upfront: if you pay more AMT tax than you owe in regular tax, you don't get the difference back as a refund. The AMT credit can only be applied against future tax liability when your regular tax liability exceeds your AMT liability.

Let’s say you exercised ISOs a few years ago and paid $50,000 in AMT. At the time, your regular tax was lower, so you couldn’t use that credit yet.

Fast forward to a big liquidity event: you sell your shares and owe a large capital gains tax bill. In that year, your regular tax is finally higher than your AMT. That’s when you can start using your AMT credit, reducing your tax bill by drawing down that $50,000 over time.

AMT credit isn’t something you apply for separately, it’s something you generate, track, and claim over time through your tax filings.

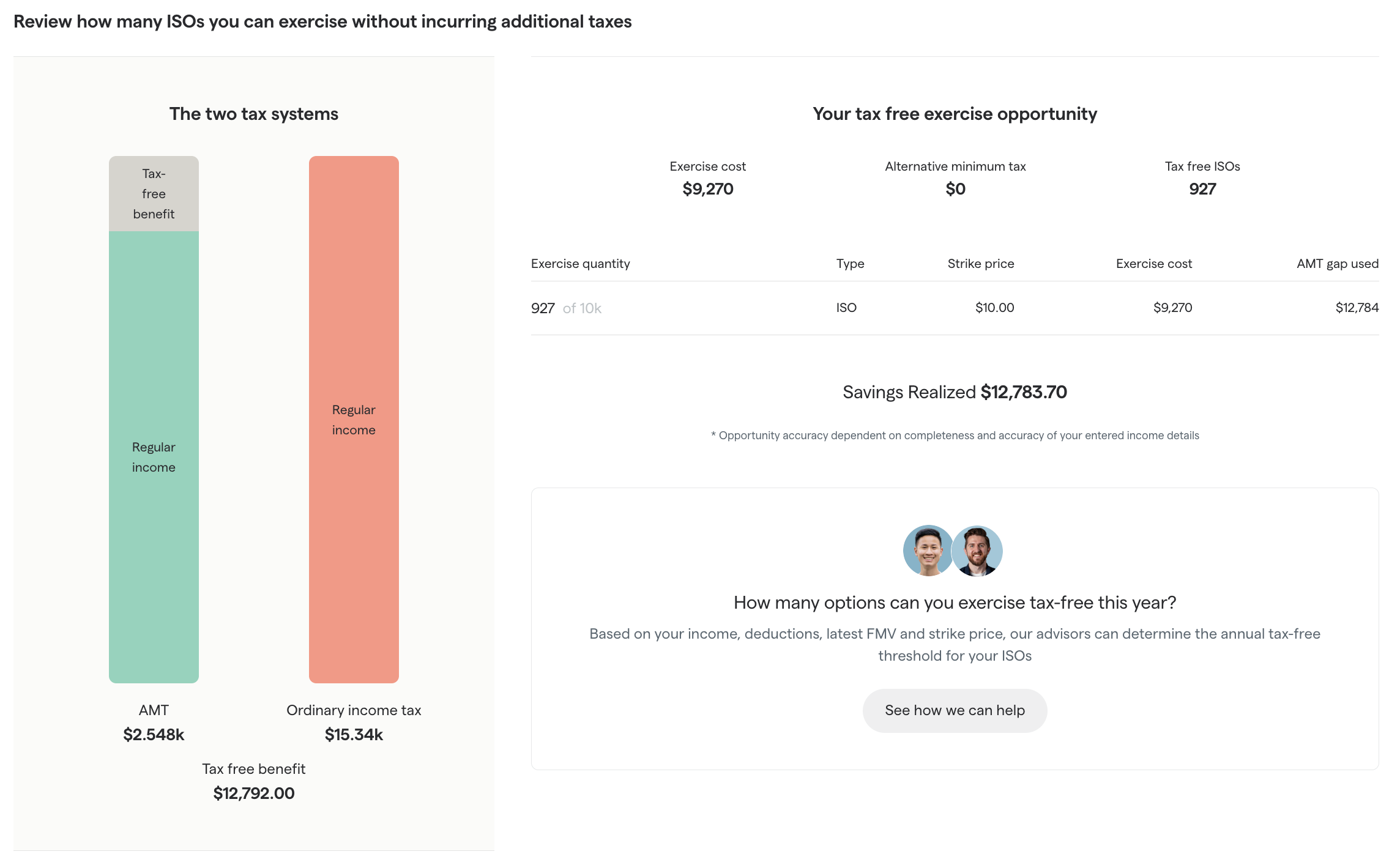

In this example, an ISO exercise triggers a $70k AMT bill vs $50k in the standard system. Because the AMT is higher, you must pay $70k. The extra $20k you pay becomes your AMT credit to carry forward.

For illustrative purposes only. Actual results may vary and there is no guarantee of any particular outcome.

If you’ve paid AMT in a prior year (most commonly after exercising ISOs), here’s how the process works:

Start by reviewing the tax return from the year you exercised your stock options.

Look for:

If AMT was triggered, the difference between AMT and your regular tax becomes your AMT credit.

AMT credit can carry forward indefinitely under current tax law, so it’s important to understand how much you still have available.

Review prior tax returns to see whether you’ve already used part of the credit, and how much remains unused. This is often tracked on Form 8801 (Credit for Prior Year Minimum Tax).

Each tax year, you can apply AMT credit when filing your taxes, but only if your regular tax exceeds your AMT for that year.

To claim it you complete and file Form 8801 with your tax return, calculate how much of the credit you’re allowed to use that year and then reduce your tax bill accordingly.

Most filers won't use the full credit in one year. Any unused portion becomes an AMT credit carryforward that rolls into future years and can be used whenever your tax calculation allows.

AMT credit recovery often happens gradually over multiple years.

That’s why it’s important to maintain a clear record of your remaining credit, work with a tax professional or equity strategist if your situation is complex and model future scenarios (e.g. liquidity events) to understand when you’ll recover the full amount.

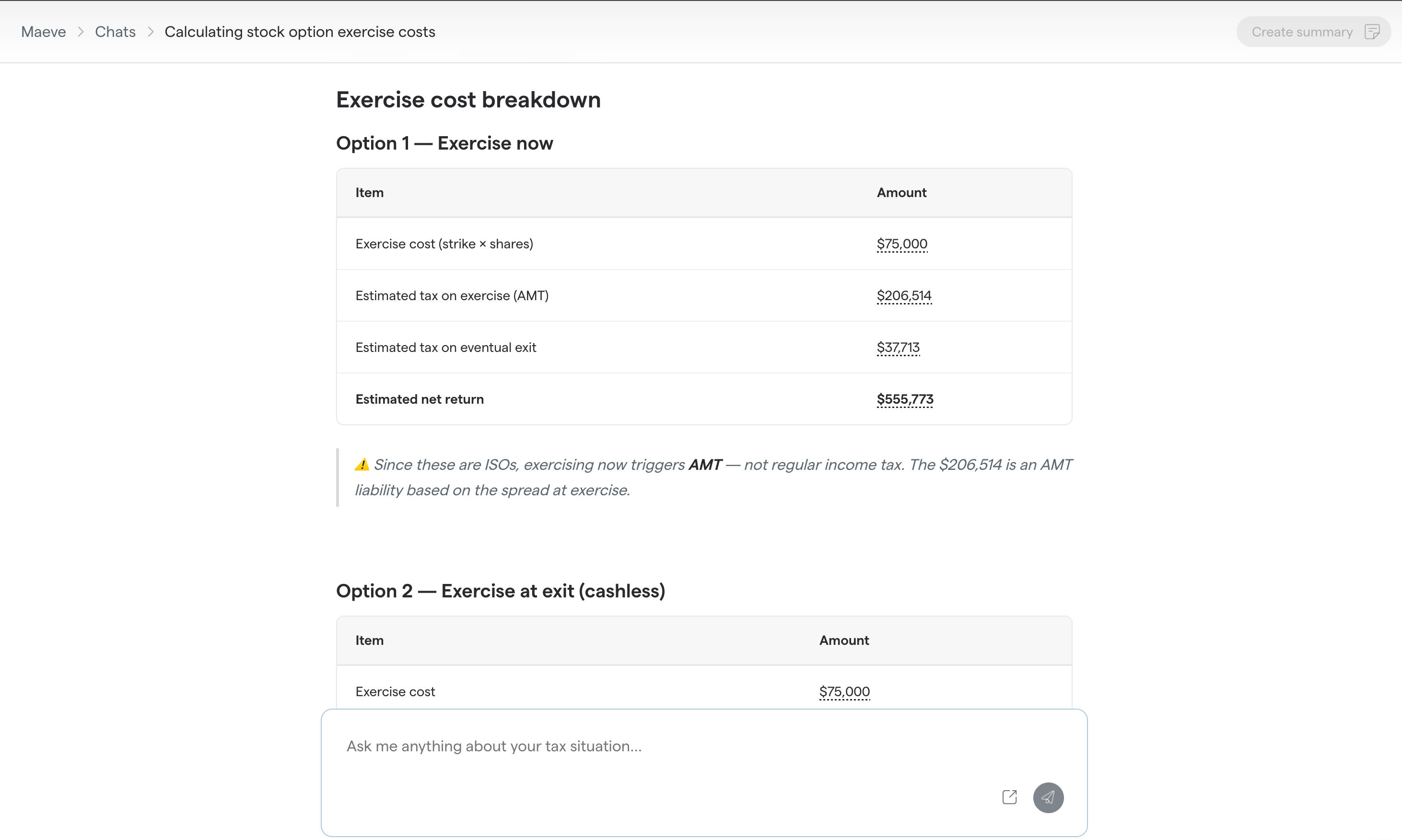

The best way to showcase the calculation is to go through an example (however, note that these are always estimates until you work with an equity strategist or tax preparer).

Say you have 25,000 options and you are ¾ of the way through your vesting schedule (so 18,750 options have been vested so far).

You may be interested in calculating how much it will cost to exercise all your vested options vs the cost to exercise all the options you have.

There are 2 ways to calculate this:

If you want a faster, more accurate way to estimate your AMT and potential credit, using a dedicated tool can make a big difference.

At Secfi, we built Maeve, an AI equity assistant, to help tech employees model these scenarios with more precision. Instead of relying on generic assumptions, Maeve uses your actual tax and equity data to give you a clearer picture of what your AMT liability could look like.

Maeve connects to your data sources (such as company and market data) and uses Secfi’s proprietary financial engines to run calculations grounded in real inputs. With various features such as verified values and data trails, you can verify where key values come from and understand how each assumption impacts the outcome.

You can import your equity from Carta, upload grant documents, or enter your details manually, along with your tax profile. Maeve supports all major equity types, including ISOs, NSOs, RSUs, and shares, and tracks key factors like vesting, exercise costs, and tax implications.

For illustrative purposes only. Actual results may vary and there is no guarantee of any particular outcome.

From there, you can model different scenarios side by side, for example, exercising now vs later, or planning around a potential exit, so you can understand how each decision impacts your taxes and outcomes.

Because AMT involves many moving parts, your final numbers will still depend on your tax filing. But Maeve helps you plan ahead with more clarity, so you’re not making decisions blindly.

Using Secfi is the fastest way to run these calculations, but if you prefer to understand the mechanics or build your own model, you can estimate your AMT and potential credit with a simple spreadsheet.

Just keep in mind this is an approximation, for exact numbers, it’s best to work with a tax advisor.

This is the key driver of AMT when exercising ISOs, it represents the “paper gain” you’re taxed on.

Formula: Bargain element = (409A value – strike price) × number of shares exercised

Using the example:

Bargain element = ($10 – $2) × 18,750 = $8 × 18,750 = $150,000

Next, add the bargain element to your ordinary income to estimate your AMT income.

Formula: AMT income = regular income + bargain element

If your salary is $200,000:

AMT income = $200,000 + $150,000 = $350,000

You can then subtract the AMT exemption (this changes year to year) to estimate your taxable income under AMT. This exemption phases out at higher income levels, but you can use a rough estimate:

Formula: Taxable AMT income = AMT income – exemption

Example (single filer):

$350,000 – $81,300 = $268,700

Apply AMT tax rates to your taxable AMT income:

Approximation:

AMT ≈ ($220,000 × 26%) + (remaining × 28%)

Now compare your AMT to your regular tax liability.

Example:

Extra AMT paid = $25,000, then this becomes your AMT credit

In future years, you can recover this credit, but only partially each year.

Formula: AMT credit usable = regular tax – AMT (in that future year)

Example next year:

You can use $5,000 of AMT credit that year

Remaining credit carries forward:

$25,000 – $5,000 = $20,000 left

Once your spreadsheet is set up, you can start testing different strategies to see how they impact your taxes over time.

For example, you might model:

Unfortunately, the AMT credit is not as simple as paying the tax in year one and claiming a refund of the entire amount in year two.

Instead, the amount of AMT credit you can take in a given year is limited to the amount that your regular tax liability exceeds your AMT calculation in that given year.

AMT credit in a given year is limited.

Given the limitation, it may take you years to recover the AMT credit depending on how big the initial bill was. But don’t worry too much, if your company has a successful exit, you will likely be able to recover the rest of the AMT credit in the year you sell your shares.

It’s worth noting that this limitation also means that you cannot claim any AMT credit in a year that you generate the AMT, so you must plan your stock option exercises accordingly to ensure that you maximize your benefit.

Source: Topic no. 556, Alternative Minimum Tax (irs.gov)

At Secfi, we help employees at growth-stage companies navigate one of the most complex parts of equity compensation: deciding when and how to exercise stock options in a tax-efficient way.

Through a combination of planning tools, expert guidance, and financing solutions, we help you understand your options, model different scenarios, and make decisions with confidence, without being caught off guard by taxes like AMT.

You can start by signing up for free to access our equity planning platform, where you can model your AMT exposure and exercise strategy. If you decide to move forward, we can also help you finance the cost of exercising your options or covering your AMT bill.

Here are a few reasons why employees at companies like Coinbase, Databricks, and Anduril choose to work with Secfi:

Although there are plenty of financial modeling tools on the market, very few are built specifically for equity compensation.

Planning around stock options is fundamentally different and more complex than modeling traditional investments. This is because most generic tools assume liquid assets, predictable returns, and clear timelines. With equity, you are dealing with uncertain exit timing, changing valuations, and tax implications that do more than affect the outcome.

In many cases, tax drives the entire strategy. You also need to factor in inputs like strike price, 409A valuations, and vesting schedules, which most tools are not designed to handle.

That is why it is important to use a platform that understands these nuances and helps you optimize for taxes, not just returns.

That’s where Secfi comes in. Maeve is designed specifically for equity planning, bringing together your data, tax modeling, and scenario analysis in one platform. You can import your equity directly from Carta, upload documents, or enter details manually. From there, Maeve helps you:

For illustrative purposes only. Actual results may vary and there is no guarantee of any particular outcome.

Instead of juggling multiple spreadsheets, this allows you to model different scenarios in one place and clearly see how each decision impacts your taxes and outcomes over time.

One of the biggest challenges with AMT is timing. Many employees only realize they owe it when the amount is already significant.

In an ideal scenario, you would exercise your options earlier, when the gap between your strike price and the 409A valuation is smaller. But earlier in a company’s journey, exercising can feel risky because there is no guarantee the valuation will continue to rise.

This is why many tech employees get caught off guard. You decide you want to exercise your options, but the combined cost of the shares and the tax bill is too high to cover with cash on hand.

This exact problem is what led to the creation of Secfi. Our own founders wanted to exercise their options at the company they worked for, and yet they didn’t have the capital to do so.

With Secfi, you can access non-recourse financing to cover both the cost of exercising your options and any associated taxes. Because the financing is non-recourse, you do not need to use your personal assets. Instead, your shares are used as collateral.

If your company’s valuation decreases, you are not personally liable. If there is a successful exit, repayment comes from the proceeds. You only repay the amount financed plus a fee when your company goes public or is acquired, and there are no payments required before that point.

This structure allows you to retain ownership and potential upside, without taking on the risk of a traditional loan. Secfi is also an SEC-registered broker-dealer and a member of FINRA and SIPC, providing an added layer of regulatory oversight.

If you believe your company’s value will continue to grow, exercising earlier can help limit future AMT exposure. Financing can make that decision more accessible by removing the upfront cash constraint.

If you are interested in exploring financing options, you can learn more about Secfi’s non-recourse financing here: Get financing for your pre-IPO options and shares

Even with the right calculators and models, it can still be difficult to determine the best decision for your specific situation. Your strategy may depend on factors like whether you plan to leave your company soon, buy a home, or hold your shares for several years until a liquidity event.

With Secfi, you get access to a team of specialists who work with stock options every day. Our equity strategists and tax experts have deep experience helping employees navigate complex decisions around exercising, taxes, and timing.

If you want more comprehensive support, you can also work with our wealth management team. They can help you build a financial plan that aligns with your goals, create a tailored investment portfolio, and develop a clear strategy for managing your equity over time.

You can learn more here: Get access to wealth advisors specialized in equity planning

When Amanda joined a fast-growing unicorn software company, she didn’t fully understand how stock options worked or what the tax implications would be.

The company gave every employee that had been there for at least 3 years the option of converting their incentive stock options (ISOs) to non-qualified stock options (NSOs). By doing so, employees wouldn’t lose their options if they left the company, which seemed like a good idea.

But Amanda wasn’t sure if it was the right move. As she started running the numbers, she realized that while NSOs offered more flexibility, they came with less favorable tax treatment compared to ISOs.

The more she learned about AMT and capital gains tax, the more complex the decision became. She found herself weighing two main options:

That is when she reached out to Secfi.

Working with Vieje, Secfi’s Director of Equity Strategy, Amanda was able to better understand the tax implications of exercising. She learned that exercising ISOs earlier could help reduce her AMT exposure and improve her long-term tax outcome.

As she put it, “Secfi was one of the only websites I could find that could give me accurate calculations of AMT.”

Instead of taking on a traditional loan, Amanda chose to finance her exercise through Secfi. This allowed her to move forward without putting her personal finances at risk, while still maintaining ownership and upside in her shares.

The structure made sense for her situation. She would only repay the financing if there was a successful exit, and if the company never went public or was acquired, she would not owe anything.

You can read the full story behind her decision here: Why a startup employee used Secfi to buy her stock options.

Testimonials are specific to an individual Client’s experience and may not be representative of all Clients. Unless otherwise indicated, Clients offering a Testimonial do not receive compensation and their statement does not present a conflict of interest.

AMT is one of the most complex parts of exercising stock options, and it often catches people off guard. It is not something that only applies to a small group of employees. In reality, many tech employees encounter AMT at some point, and the amounts involved can be significant.

The key is not just understanding whether you might owe AMT, but planning for it ahead of time. When you do, AMT becomes something you can manage, rather than something that surprises you.

With the right tools and guidance, you can model your exposure, understand your potential AMT credit, and make more informed decisions about when and how to exercise.

If you want to get a clearer picture of your situation, you can start by using Secfi’s AI calculator Maeve and signing up to the platform to get an estimate of what you would owe: Get started.

AMT credit is a tax credit you receive after paying alternative minimum tax in a prior year. It allows you to reduce your future tax bills by the extra amount you previously paid under AMT.

No, AMT credit is not paid out as a cash refund. It can only be used to offset future taxes, and only in years when your regular tax liability is higher than your AMT.

It depends on your income and tax situation. Many people recover AMT credit gradually over several years, although a liquidity event like an IPO that allows you to sell your shares can accelerate recovery.

You generate AMT credit in any year where your AMT liability is higher than your regular tax. This often happens when you exercise incentive stock options (ISOs) and hold the shares without selling them.

Under current tax law, AMT credit does not expire. Any unused credit carries forward indefinitely until you are able to use it against future tax liability.

The tool shown here uses artificial intelligence and is for illustrative purposes only and not necessarily indicative of future results and there is no guarantee that similar results can be achieved. The information provided by the tool is not professional advice and is not intended by Secfi, Inc., its affiliates, and Secfi representatives, to be deemed as investment, legal, tax or other professional advice or recommendations of any kind, or to form the basis of any decision to do or to refrain from doing anything. Secfi does not review the accuracy or completeness of the information provided to us within the tool.