What is the alternative minimum tax (AMT) and how does it work?

2 min

0 result

The alternative minimum tax (AMT) is a special tax you may owe when exercising incentive stock options (ISO).

It’s a tax system to ensure high-income taxpayers pay the adequate amount of federal income tax. The system limits certain tax benefits, exclusions, and tax deductions so taxpayers can't stack too many loopholes and drive their tax liability down to almost nothing.

With AMT, you’ll calculate your tax liability twice: via the regular tax system and via the AMT rules. The highest of the two is the one you’ll pay.

To prevent an unexpectedly high tax bill, make sure to check whether this applies in your case before exercising ISO.

In this article, we’ll cover:

Note: Secfi provides equity planning experience, tools and financing so startup employees can own their stock options with confidence. If you’re looking to better understand what you can do with your equity, sign up to our platform here: Get Started

The AMT calculation uses a different set of tax rules than regular income tax. Because the AMT system strips away certain itemized deductions and credits, it often produces a higher taxable income and a higher tax bill.

Some key differences include:

For tech employees, the reason AMT comes up is due to the unique rules around stock options. If you exercise your ISOs and don’t sell them in the same year, the spread between what you paid for the options and the Fair Market Value (FMV) of the stock is seen as income taxed by AMT.

AMT tends to affect people who:

Calculating AMT will always be an estimate until you work with an equity planner. There are many variables involved, and your situation may differ significantly from someone else’s.

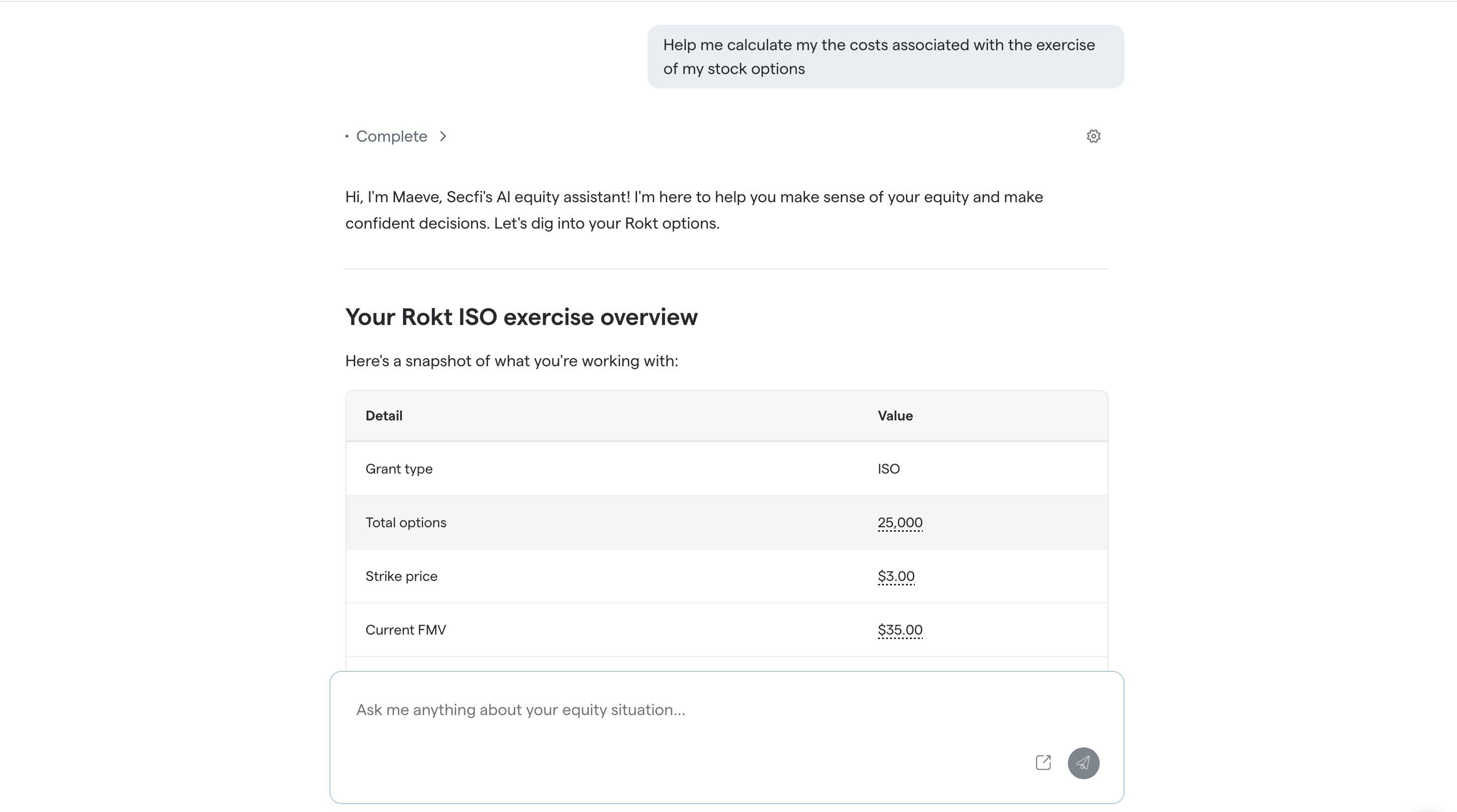

At Secfi, we built Maeve to help tech employees model these scenarios with more precision. Instead of relying on generic assumptions, Maeve uses your actual financial and equity data to give you a clearer picture of what your AMT liability could look like.

Maeve connects to your data sources and uses Secfi’s proprietary financial engines to run calculations grounded in real inputs. With various features, you can verify where key values come from and understand how each assumption impacts the outcome. It combines the flexibility of AI with the reliability of Secfi’s tax calculation engine.

Maeve also incorporates regularly updated data, including 409A valuations and secondary market insights, so your models reflect a current view of your portfolio.

To get started, you can import your equity grants directly from Carta, upload your grant documents, or enter your details manually. You can also input your tax profile so Maeve can run calculations tailored to your situation instead of relying on broad assumptions.

It supports all major types of equity, including ISOs, NSOs, RSUs, and shares, and tracks vesting schedules, exercise costs, and tax implications such as AMT so you can compare different strategies side by side. Your data is encrypted and used only to power your experience within Secfi, and is not sold to third parties.

AMT itself is calculated in parallel to your regular tax system using a different set of rules. Each tax year, you are required to calculate both your regular tax liability and your AMT, and you pay whichever amount is higher.

Because this involves many moving parts, tax preparation software or an accountant usually handles the actual filing. Maeve helps you understand and model these outcomes ahead of time so you are not caught off guard.

For illustrative purposes only. Actual results may vary and there is no guarantee of any particular outcome.

You can also estimate your AMT manually using a spreadsheet, working through the same logic the IRS uses on Form 6251. To do this, you will first need to gather a few key inputs:

Once you have these, calculate your AMT adjustment, also known as the spread. These adjustments are part of a broader category the IRS calls preference items:

Spread = (FMV – Strike Price) × Shares Exercised

Then, compute your alternative minimum taxable income (AMTI):

AMT Income = Regular Taxable Income + ISO Spread

Then subtract the AMT exemption. This step gets more complex at higher income levels, since the exemption begins its exemption phaseout once your income crosses certain limits:

AMT Taxable Income = AMT Income – Exemption

Once you have your AMT taxable income, apply the AMT tax rates:

This can be expressed as:

(Threshold × 0.26) + (AMT Taxable Income – Threshold) × 0.28

The result is your tentative minimum tax. Your final calculation would be:

AMT bill = AMT tax – Regular tax

If the AMT calculation is higher, that's what you'll owe for the year. You'll report it on your Form 1040 as part of your annual tax filing, with the supporting math on IRS Form 6251.

It is also important to know that any excess AMT you pay is not lost. It can potentially be recovered in future years as an AMT credit when your regular tax exceeds your AMT, which you’ll claim using Form 8801. This is just an example, it’s important that you speak to a tax professional regarding your particular circumstance.

Read more here: What is AMT credit and how does it work?

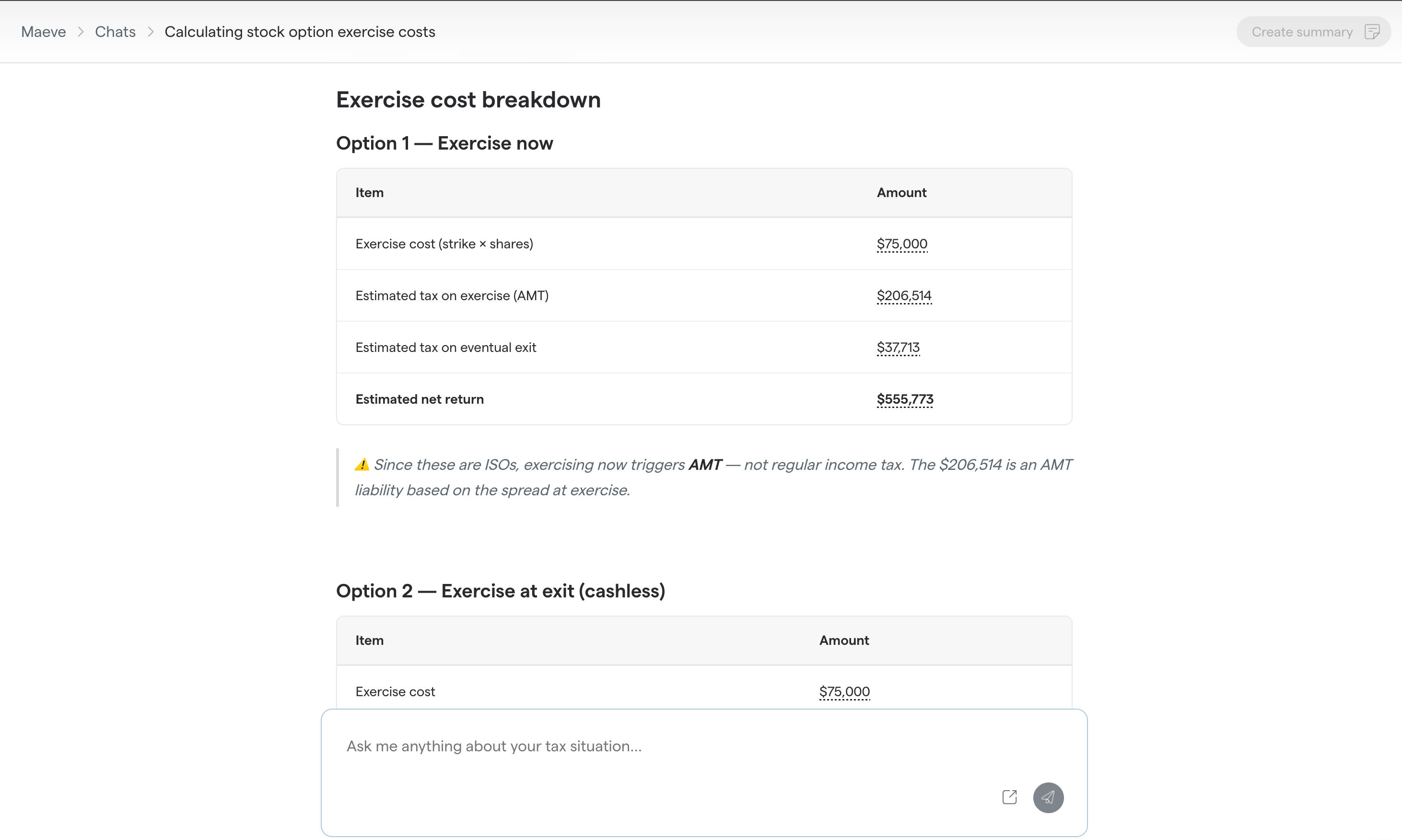

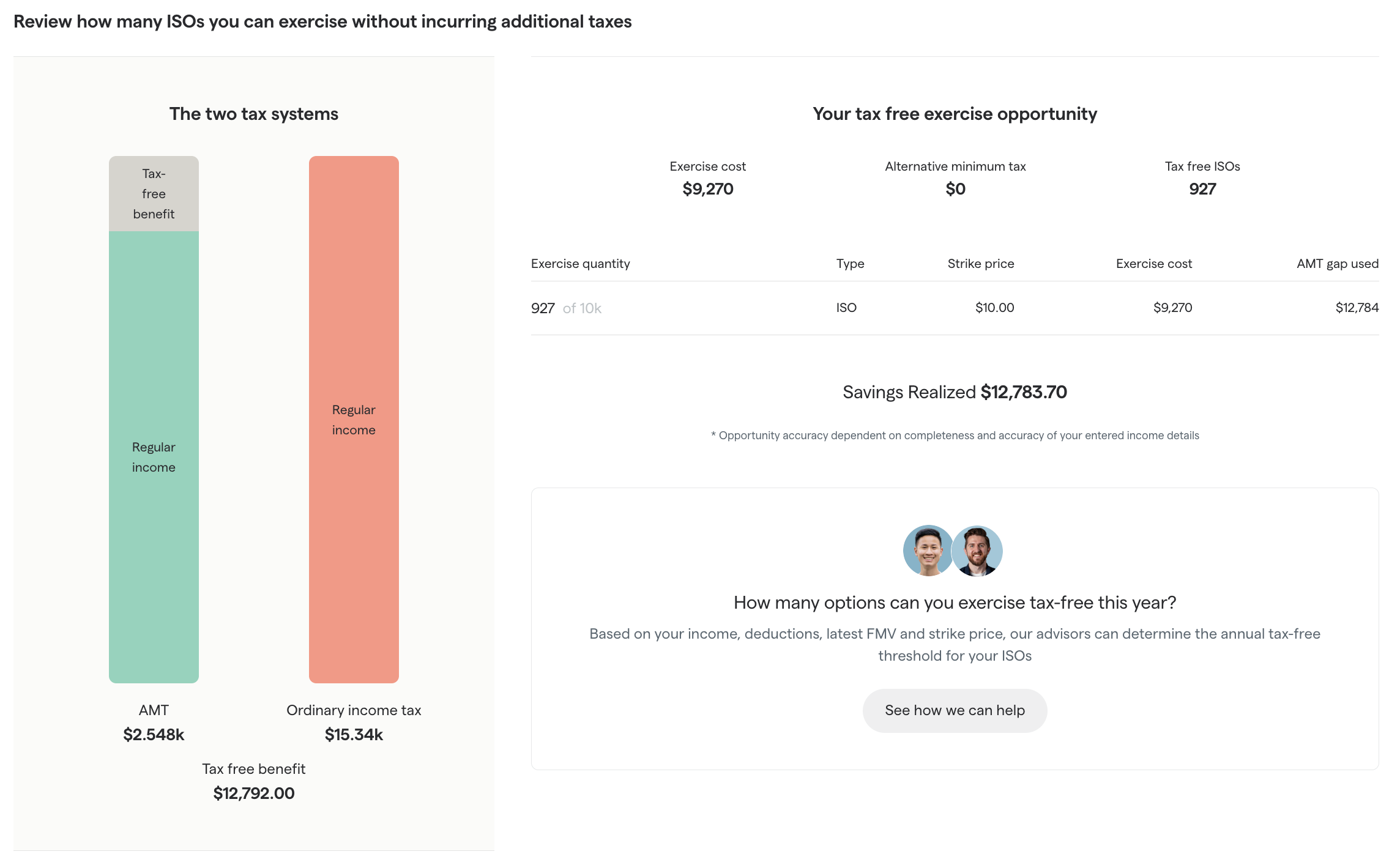

There are ways to plan your option exercise that can reduce or even avoid triggering AMT.

At Secfi, we built Maeve to help you model these decisions before you act. Maeve includes a built-in calculator specifically designed to show how many ISOs you can exercise without triggering AMT in a given year, based on your actual equity and tax profile.

Instead of guessing, you can see how different exercise amounts impact your potential AMT liability and adjust your strategy accordingly. This allows you to see how changes in timing, number of shares, or strategy affect your tax outcome.

For illustrative purposes only. Actual results may vary and there is no guarantee of any particular outcome

In general, AMT is triggered when the spread from exercising ISOs becomes large enough. If you exercise a smaller number of options, you may be able to stay below the AMT threshold.

There are also broader ways to reduce your AMT exposure, such as potentially lowering your taxable income, helping maximize retirement contributions, or increasing charitable giving in the same year.

Because these decisions involve trade-offs and depend heavily on your personal situation, it is worth speaking with a tax advisor or equity planner. Tools like Maeve can help you explore your options, but a professional can help you build a strategy that aligns with your goals.

The AMT credit works a bit like a delayed rebate. You may pay more tax upfront under AMT, but some of that extra amount can be recovered in future years.

This happens because AMT can tax you on “paper gains,” such as shares you have exercised but not yet sold. The credit exists to prevent you from being taxed twice on the same income, once when you exercise and again when you eventually sell the shares.

However, the credit is not refunded immediately. You can only use it in future years when your regular tax exceeds your AMT. Even then, it is typically recovered gradually rather than all at once.

In this example, an ISO exercise triggers a $70k AMT bill vs $50k in the standard system. Because the AMT is higher, you must pay $70k. The extra $20k you pay becomes your AMT credit to carry forward.

For illustrative purposes only. Actual results may vary and there is no guarantee of any particular outcome

Because of this, it is important to track your AMT credit over time. Reviewing it each year with a tax advisor or equity strategist can help ensure you fully use the credit when the opportunity arises.

Read our full article on this here: What is AMT credit and how does it work?

The AMT is a parallel tax system meant as a fallback to prevent excessive tax avoidance.

Back in the 1960s, some Americans got so good at legally not paying taxes that Congress enacted the AMT in 1969. Instead of going through the trouble of fixing the tax code and closing loopholes, federal lawmakers decided that this patch was a better solution.

The vast majority of Americans will never encounter the AMT. Unfortunately for startup employees, one of the factors that drives up your AMT is the exercise of ISO.

While not normally taxed, exercising ISO does increase your AMT. Exercising enough ISO may put your AMT above your regular tax liability, forcing you to pay the additional tax.

At Secfi, we combine equity planning expertise, tools, and financing to help startup employees own their stock options with confidence.

If you’re confused by AMT, you’re not alone. This is a tax we deal with every day when working with tech employees, from early-stage hires to late-stage executives. We understand the nuances of equity compensation and how AMT fits into the bigger picture.

Here’s how and why tech employees across the US work with us:

As a tech employee, you’re in a unique position. You have to think about equity, strike prices, taxes, and timing all at once. Most financial tools are not built for this level of complexity, which makes it difficult to understand your options and make confident decisions.

Our founders were once in the same position, navigating stock options without the right tools to properly plan for them, which is what led them to start Secfi.

That’s why we built Maeve. Instead of juggling multiple calculators and spreadsheets, Maeve gives you a single platform to understand your full financial picture. You start by inputting your equity and tax details, and Maeve uses that information to model scenarios tailored to your situation.

Because it is built specifically for tech employees, Maeve can help you understand:

Rather than relying on generic outputs, you get insights based on your actual data. It is one of the most comprehensive ways to understand and plan around your equity, all in one place.

You can sign up for free here: Get Started

For illustrative purposes only. Actual results may vary and there is no guarantee of any particular outcome

Tools like Maeve are a great place to start, but at some point, your questions become more specific to your situation:

This is where working with a tax advisor or wealth manager becomes important. But not all advisors are equipped to handle the complexities of equity compensation. You want someone who understands how stock options, taxes, and liquidity decisions all fit together.

At Secfi, this is our focus. Our team works with equity every day, and we also have a dedicated investments team with deep experience in venture capital and company valuations.

By working with our wealth managers and certified financial planners, you get a financial plan tailored to your goals, an approach that evolves with your situation, and a portfolio designed to complement your career and equity position.

You’ll also be working with a Regulated Investment Advisor (RIA) with aligned incentives. Our compensation is based on transparent fees, not commissions or kickbacks.

You can learn more about how this could help you here: Get Financial Advice

What if you calculate your AMT bill and realize that exercising your options, plus the tax, is more than you can afford?

This is where non-recourse financing can help. It allows you to access the cash you need to exercise your options and cover taxes, without putting your personal assets at risk and while retaining full ownership of your shares.

There are no monthly payments. You only repay the financing if and when your company exits, such as through an IPO or acquisition. If the company does not succeed, you are not required to repay it.

For many tech employees, this is a way to participate in the upside of their equity without committing significant personal capital upfront.

We’ve worked with employees from companies like Gusto, Databricks, and Anduril to help them exercise their options and manage the associated costs.

You can learn more about non-recourse financing here: What is non-recourse financing for stock options?

In the past, Austin felt unsure about how to approach equity planning. At his first company, he used the proceeds from his equity for practical goals like paying off student debt and buying a home.

When he joined a new company that had reached unicorn status, his mindset shifted. With a young family and a longer-term outlook, he wanted to better understand his equity and how it could support his future goals.

He started looking for a financial advisor, but quickly realized that even experienced advisors, including friends in the field, did not fully understand stock options or the tax implications. He struggled to get clear answers to important questions.

As he put it, “I remember telling my wife that I feel like I’m wading into new waters here. If we get this wrong, it could either cost us a lot in taxes now or thousands of dollars down the road.”

Austin discovered Secfi through its tools and learned that the team also offered specialized equity planning advice. He was looking for guidance on tax planning, especially given his commission-based income, and how to manage his portfolio after a potential exit.

“The question I had about taxes at the end of the year is only going to turn into another question, and another question,” he said. “And every single one of them could have a big impact if I get it wrong. That’s why I decided to work with them.”

Secfi helped him build a clear, multi-year plan. This included determining how many shares to exercise each year, specifically exercising ISOs up to the AMT threshold, and planning future exercises to make the most of AMT exemptions while minimizing taxes over time.

“I don’t know that any other financial advisor would say, ‘you should exercise this many options and set aside this much in taxes because that’s better for you long term,’” he said. “That’s the type of guidance I was looking for.”

With a structured plan in place, Austin now understands when to exercise, what it will cost, and how much to set aside for taxes, giving him confidence that his equity strategy aligns with his broader financial goals.

You can read the full story here: Why a startup sales director hired a financial advisor to make better equity decisions

Testimonials are specific to an individual Client’s experience and may not be representative of all Clients. Unless otherwise indicated, Clients offering a Testimonial do not receive compensation and their statement does not present a conflict of interest.

AMT is a tax that often catches tech employees off guard. You may think you have enough cash to exercise your options, only to realize later that the tax bill makes it much more expensive than expected.

With the right planning, you can be more intentional about how many shares you exercise and when, helping you manage or minimize your AMT exposure.

And if covering the upfront cost is a challenge, options like non-recourse financing can allow you to move forward without tying up your personal capital, while still participating in the upside of your equity.

The key is understanding your situation early and building a strategy that works for you.

You can sign up to Secfi for free here to model your AMT and explore your options: Get Started

No. You only pay AMT if your AMT calculation is higher than your regular tax. This typically happens when the spread between your strike price and the fair market value is large enough. If you exercise a smaller number of shares or sell them in the same year, you may avoid triggering AMT.

The best way is to model your situation ahead of time. Because AMT depends on factors like your income, filing status, and the size of your option exercise, it is difficult to estimate manually. Tools like Maeve can help you simulate different scenarios so you can understand the potential tax impact before making a decision.

If the cost of exercising your options and paying AMT is too high, you still have options. Some employees choose to exercise fewer shares or adjust the timing. Others use solutions like non-recourse financing to cover the upfront costs without using personal funds, allowing them to participate in the potential upside of their equity.

The tool shown here uses artificial intelligence and is for illustrative purposes only and not necessarily indicative of future results and there is no guarantee that similar results can be achieved. The information provided by the tool is not professional advice and is not intended by Secfi, Inc., its affiliates, and Secfi representatives, to be deemed as investment, legal, tax or other professional advice or recommendations of any kind, or to form the basis of any decision to do or to refrain from doing anything. Secfi does not review the accuracy or completeness of the information provided to us within the tool.