🫧 What to do when the AI bubble pops

0 result

Mike’s a CPF® at Secfi. He specializes in helping clients make the most of their stock options and integrate equity compensation into their broader financial plans.

You’re sitting on the sidewalk as the heat of the mid-summer sun beats down on you and you playfully reach for the little plastic wand of soapy water. Exhaling, you slowly inflate with a mix of childhood excitement and quiet anxiety wondering whether this will be the biggest and best bubble yet. Time slows to what feels like an eternity. And suddenly, but expectedly, the bubble pops. In hindsight, the fragility of it all felt so obvious.

Eric here this week and as an advisor, I can’t help but recognize how we’ve been here before. Market participants constantly wondering if we’re in a bubble. As if the explosive upside we’ve seen in the stocks of fabless chip designers and memory manufacturers can continue indefinitely and this time is different.

As Jeremy Irons’ character John Tuld so aptly notes in Margin Call, “It's certainly no different today than it's ever been. 1637, 1797, 1819, 37, 57, 84, 1901, 07, 29, 1937, 1974, 1987-Jesus, didn't that f* me up good-92, 97, 2000 and whatever we want to call this. It's all just the same thing over and over; we can't help ourselves.”

No, we can’t. Innovation breeding excitement, bringing fervor, leading to overhype - all of which eventually meet reality.

So if we’ve seen this playbook before, what should you do about it? Some questions I’ve been fielding are:

Within the list of years rattled off by Tuld is the famous Dutch Tulip mania, the land speculation bubble of 1797, railroad-induced bubbles and panics 1884 and 1901, and of course the dot com bubble.

In more recent history, I’d point to hype cycles you probably recall like the 2017 Initial Coin Offering (ICO) boom and bust, the 2018 cannabis hype that went up in smoke, and the 2020 crypto/NFT/metaverse pipedream that woke up once interest rates crept above 0%.

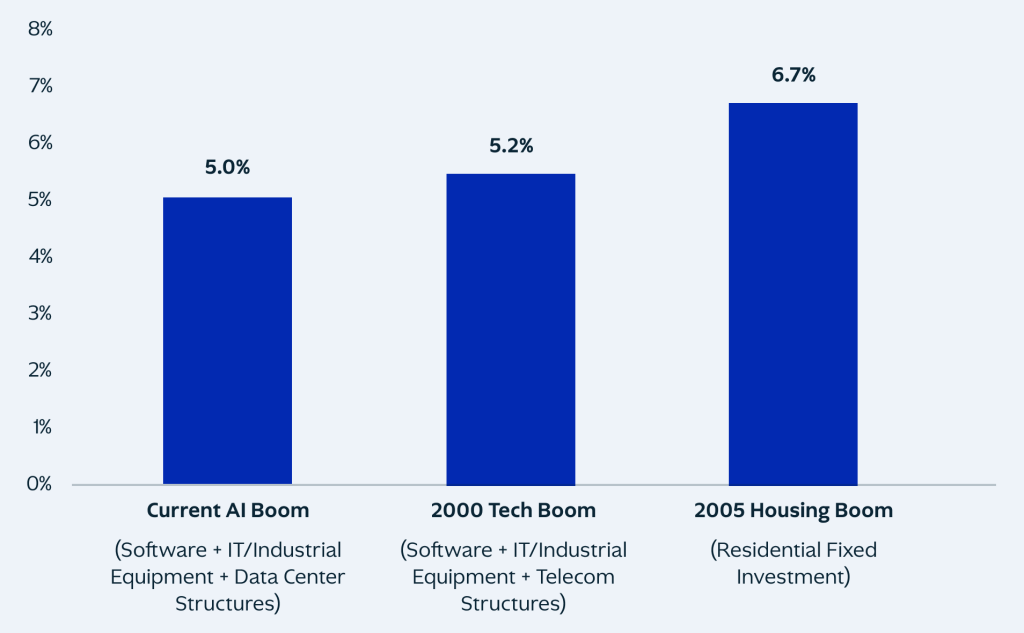

So where are we today? Capital expenditure on AI is rivaling the spend on past booms:

Investment Spend as % of U.S. GDP

Past Performance is not indicative of future results.

In the current AI boom, a large portion of investment is a picks and shovels play (a common refrain tying back to the gold rush, noting that some of the best investments came from the tools used to mine gold rather than the gold itself). In this case, the infrastructure generating the compute rather than how the compute is used.

Beyond the infrastructure are the AI labs and startups looking to disrupt every industry under the sun. The trend has been escalating. Using YCombinator funded companies as an indicator for startup focus and early stage VC attention, more than 85% of companies funded since 2024 have been AI focused. While Q1 2025 had a record 55% of global venture funding going to companies in the AI space, that record was shattered when it rose to 80% in Q1 2026.

There’s now a consensus view that the current US economy is one big bet on AI. Part quality capex investment. Part overzealous speculation on the technology’s potential.

The issue with financial bubbles is that, at some point, they meet the resistance of reality. Is this time different? In the ways that matter to your equity, probably not. The technology is real. The valuations are still a bet on a future that hasn't arrived yet. That's the same bet people have made over and over again.

A stock’s current valuation is the market's best guess at everything the company will ever earn, discounted back to this moment. Not just the current revenue streams, but all of the markets a company is looking to disrupt, and all the new, and future growth to come. It’s why you often see public stocks get hammered, even when they hit earnings estimates, but change their forward guidance. It’s all about effectively pricing in the future.

We feel the largest AI companies are pricing in… a lot. One could say they’re priced for perfection, or pricing in that everything is going to go right for the business. Some of these assumptions include:

On recent podcasts, Anthropic leadership has detailed the needle they’re threading. Over spend on infrastructure and compute and you bankrupt yourself. Under spend and you could fall behind. Companies need to stay ahead of all the aforementioned assumptions in order for their valuations and growth projections to hold. Should part of the AI buildout falter, we think you could see a quick cascade resulting from

While I remain optimistic on the potential, there are certainly hurdles on the innovation track ahead.

Whether we realize it or not, living within a bubble alters our thinking. Emotional contagion. Seeing headlines touting record IPOs, stock market highs, massive funding rounds drives investor sentiment. And this undoubtedly fuels our belief in the narrative around continued upside. Market melt-up.

But upon taking a step back and taking an honest look at all the assumptions that the bubble is depending on, our focus point widens enough to objectively view the whole landscape. The risk is still there. The single stock concentration still remains. The limitless upside actually has a fundamental ceiling. In our view, a bubble means you should take a pause, remove yourself from the contagion, and objectively look at your equity. Think like an investment analyst or better yet, work with an advisor, to assess the risks within your company and the market at large. The risks within your company like growth assumptions and liquidity risk tied to exit timelines. And the risks within the market such as a pullback that could cool VC funding to your space or protest efforts against data centers that could stifle industries.

Reviewing your equity in such a manner, alongside your broader financial picture and goals, will provide a better compass than viewing your equity in isolation. Especially in a time of fervor.

Assess your company against its competitors, the largest companies in the industry, and the largest companies in the world. If your company is still early stage, with a reasonable valuation, and riding a wave of adoption with years of meaningful growth ahead, your asymmetric upside likely remains intact and exercising your equity is worth exploring.

Alternatively, if your company is set to IPO as one of the 10 largest companies in the world, in a market that has brought companies public at peak valuations, it’s worth being objective about what kind of growth your equity might experience going forward.

If a tender offer presents itself, ask yourself a few questions:

In advance of an IPO lockup expiration, we think you should ask:

In either case: what are the tax implications of selling your type of equity, at this price, in this tax year, given your broader financial picture? And what are the risks in maintaining your balance sheet concentration?

The decision is deeply personal and depends on your individual financial situation, tax circumstances, and long-term goals. These are conversations worth having with a qualified financial and tax advisor before liquidity events arrive.

If history is our guide, the wake of a bubble leaves excess talent looking for opportunities, massive infrastructure that needs a new use case, and new innovations that can utilize that infrastructure in ways never imagined.

Typically, workforce displacement occurs when companies go under or shift to austerity mode to preserve capital in a downturn. This cycle is different. The very innovation inflating the bubble is being used as both cover for cutting excessive hiring in the COVID years and to replace workers. For those in the tech community impacted by layoffs, equity decisions tied to post-termination exercise windows are paramount. The question then becomes: what comes next? From vibe coding new creative projects to founding new companies, this skill base is the lichen after a forest fire, starting the rebirth of the next tech wave.

Then there’s the repricing of infrastructure. The credit and equity investors funding this buildout are exposed in ways the headlines rarely capture. Should AI revenue fail to materialize at the scale required, the losses could be severe. (Wall Street is starting to worry about AI debt) Many telecom giants and equipment suppliers of the dot com era (think WorldCom, Nortel, Lucent, Global Crossing) went under, leaving behind infrastructure that was bought for pennies on the dollar and remains the backbone of the modern internet. The 2000s dark fiber that held the capacity for YouTube and Netflix is tomorrow’s compute capacity, opening the door for the next generation of builders to access it for a fraction of the cost paid for the build out.

What to build? We think this is the creative question that will foster the future companies and innovation we use every day. Where everyone can affordably access a country of geniuses in a data center to build a company. Or use excess energy and compute to create the next new thing. Be it fun, like the next generation of immersive AR/VR with spatial computing capabilities. A resurgence of the metaverse and shared spaces in the Matrix. Helpful, like advanced training for robotics development. Or beneficial, like speeding drug discovery timelines.

After the bubble pops, we’ll be in a place where the powerful play goes on, and you may contribute a verse. What will your verse be?

Things we’re digging: