Stock options for executives: How to actually decide what to do next

3 min

0 result

San Francisco native (yes, really). @uw and Lowell High alum. I like to nerd out on fintech, stock options and taxes.

Stock options as an executive can be a major portion of your net worth, but figuring out what to do with them isn’t straightforward.

Even if you were excited at the opportunities stock options bring when you joined or started your company, today you might find yourself in a position where:

Executives in this position often find that they delay decisions, or default to just “doing nothing,” which isn’t ideal if you prefer to make more strategic choices.

This article walks through how executive stock options actually work in practice, different paths available to you, and the key decisions you’ll need to make.

Whether your priority is managing risk, accessing liquidity, or optimizing for taxes, here’s what we’ll cover:

Note: Secfi provides equity planning expertise, tools, and financing so you can make informed, confident decisions about your executive stock options. Try our secure AI tool Maeve for personalized equity, tax, and liquidity planning.

At a high level, executive stock options work the same way as any employee stock options. Mechanically, these stock options are effectively a call option on your company's underlying stock: it gives you the right (but not the obligation) to buy a set number of shares at a predetermined price (the strike price) once your options vest according to the vesting schedule in your grant.

But in practice, the risk and decisions involved at the executive level are very different.

For most executives, equity is a major part of your overall wealth, which makes the stakes much higher. Here’s what you might be noticing as you consider next steps with your executive stock options:

At a high level, most decisions around stock options for executives come down to a few core questions.

The challenge is that these choices are interconnected, and the “best” answer depends on your financial situation, goals, and how much risk you’re comfortable taking.

While you don’t need to have all of the answers right away, here’s what you might start asking yourself:

Many executives default to waiting for an IPO or acquisition, or relying on a cashless exercise when one becomes available. While these can help reduce upfront cost, they also limit your ability to control timing, manage taxes, and fully capture the upside of your equity.

We believe getting the most value from your stock options usually comes down to how you approach a few key levers: when you exercise, how you fund it, and how you manage risk and taxes along the way. In practice, most executives use a combination of the approaches below, rather than relying on a single path.

Exercising earlier in a company’s lifecycle can lower what it costs to exercise and reduce the taxes you may owe, especially if the company’s valuation increases over time. It can also help you qualify for lower long-term capital gains taxes sooner, which may help you keep more of the value if your shares increase over time.

The tradeoff is that you’re putting money in sooner and taking on more risk if the company doesn’t perform as expected.

Here’s an example to put taxes in context:

An executive might be able to exercise when the company’s fair market value is $5 per share with a $1 strike price, requiring a $500,000 upfront cost and a relatively manageable tax impact. If they wait until the fair market value reaches $20 per share, the exercise cost remains the same ($500,000). But the taxable spread increases dramatically, which could lead to a six-figure tax bill, even though the shares can’t yet be sold.

(Note that this is just an example, and it’s important that you speak to a qualified tax professional regarding your particular circumstance.)

For more considerations on when to exercise, read our guide When should you exercise your stock options?

For many executives, the biggest barrier to exercising early is the amount of cash required upfront, often with no guarantee of when you’ll actually see any liquidity.

Non-recourse financing is designed for exactly this situation. It allows you to exercise your options without using your own capital, with repayment tied to a future IPO or acquisition. Because there’s no personal liability or fixed repayment schedule, you don’t have to take on traditional debt or put more of your own money directly into the company.

For instance, instead of paying hundreds of thousands of dollars out of pocket to exercise, you could use non-recourse financing to cover both the exercise cost and taxes. If the company goes public or is acquired, the financing is repaid from the proceeds, instead of requiring you to pay it back up front.

Even employees can benefit from non-recourse financing. An executive from Happy Money used this type of financing, and was so happy with the process he brought Secfi in to provide equity education and non-recourse financing options for the entire company.

Taxes can have a big impact on how much of your equity you actually walk away with. When you exercise, how long you hold your shares, and whether you sell, all play a role in what you owe.

In some cases, exercising may trigger a big tax bill before you’ve received any cash from your shares. That can leave you in a position where you’ve already paid to exercise and still need to cover taxes out of pocket, which is one of the harder parts of managing stock options.

But if you only exercise a small portion of your options each year, you can potentially avoid or reduce your AMT tax.

For example, an executive who exercises a large number of options at once may face a six-figure tax bill in the same year, even if they can’t sell the shares yet. Planning ahead and modeling different scenarios can help reduce the chances of this happening and increase how much you keep after taxes.

Equity decisions are difficult to evaluate in your head or through rough spreadsheet estimates and generic AI tools, especially when taxes, timing, company valuations, and liquidity are all connected.

A good equity planning tool should help you model different scenarios using your actual equity and financial data, so you can compare tradeoffs more clearly and understand how different decisions might affect your outcome over time. It should also be secure, since you’re often working with sensitive financial and company information.

Maeve is a purpose-built AI for modeling your specific equity situation. We combined years of specialized tools into one easy AI equity assistant to help you model different scenarios around exercising, taxes, and liquidity using real data instead of generic assumptions.

For illustrative purposes only. Actual results may vary and there is no guarantee of any particular outcome.

Even if you understand your options, actually acting on them can be complex. Decisions around exercising, taxes, and liquidity are connected, and small changes can have a big impact on your outcome.

Secfi was built because our founders faced the same pressure. They wanted to exercise their stock options, but didn’t have the cash or appetite to take on major personal risks. Plus, it felt like there were too many factors and scenarios at play to feel confident in their decisions.

Today, Secfi helps executives and their employees navigate these situations by bringing planning, financing, and guidance into one place.

Here’s why people at companies like Stripe, Databricks, and Anduril use Secfi:

Planning around equity is very different from managing traditional investments. You’re dealing with things like strike prices, 409A valuations, vesting schedules, and uncertain outcomes, all of which can have a real impact on what you end up paying and keeping.

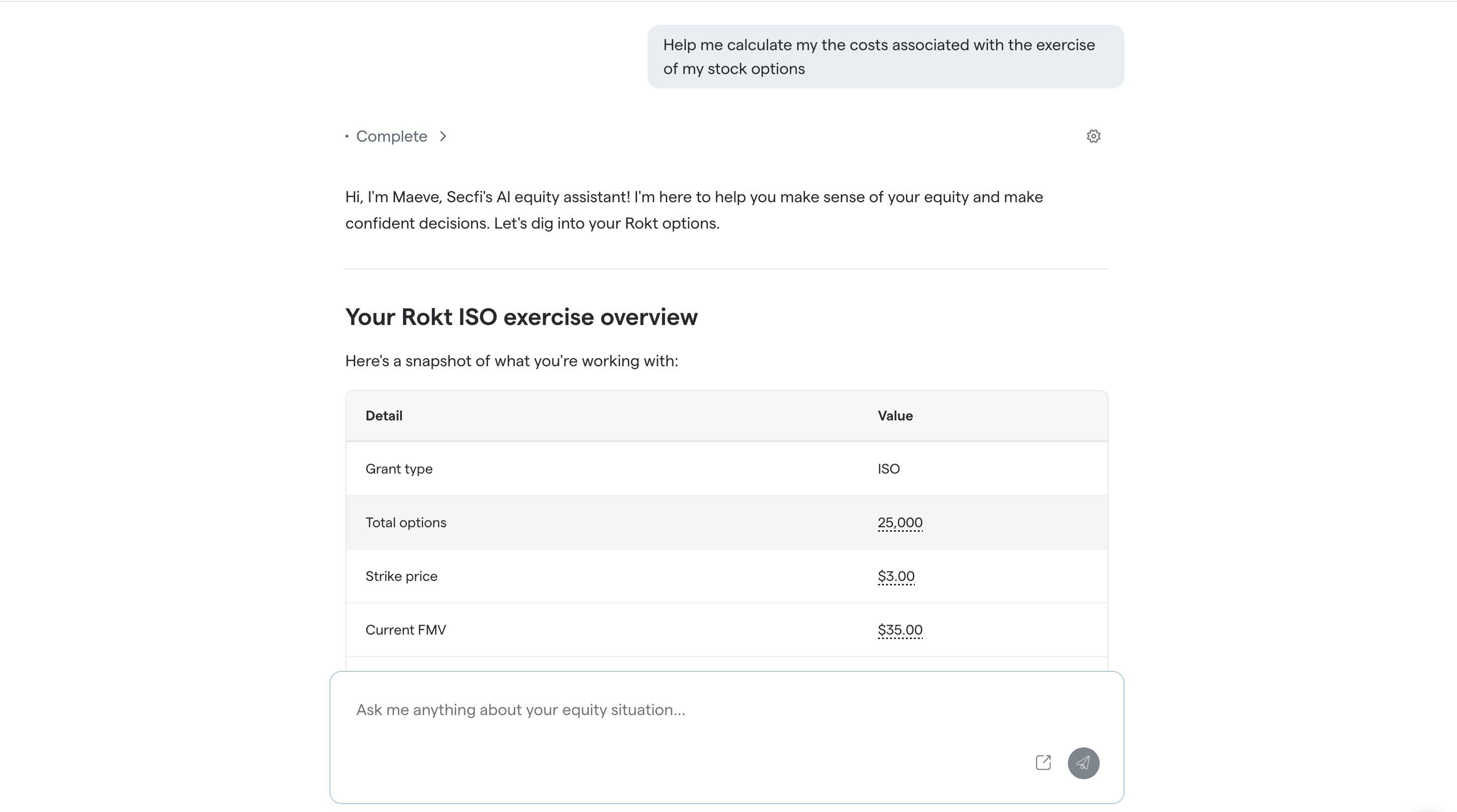

Maeve, Secfi’s AI-powered equity planning tool, lets you model different scenarios based on your specific equity and company details. It’s fully encrypted and uses your actual financial and equity data, so you’re not relying on generalizations.

You can see how decisions around timing, taxes, and liquidity might play out, and check the assumptions behind those scenarios, so you can feel more confident in the outputs.

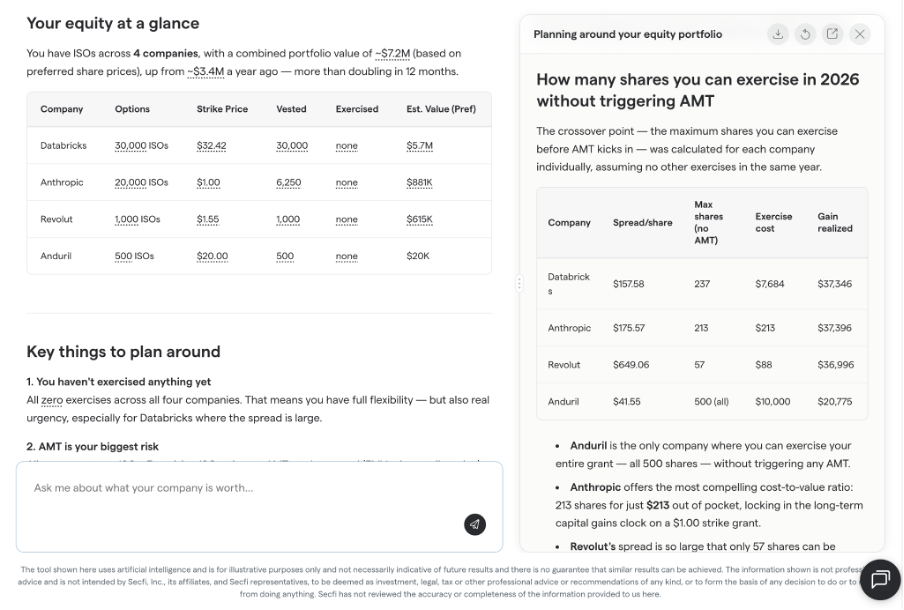

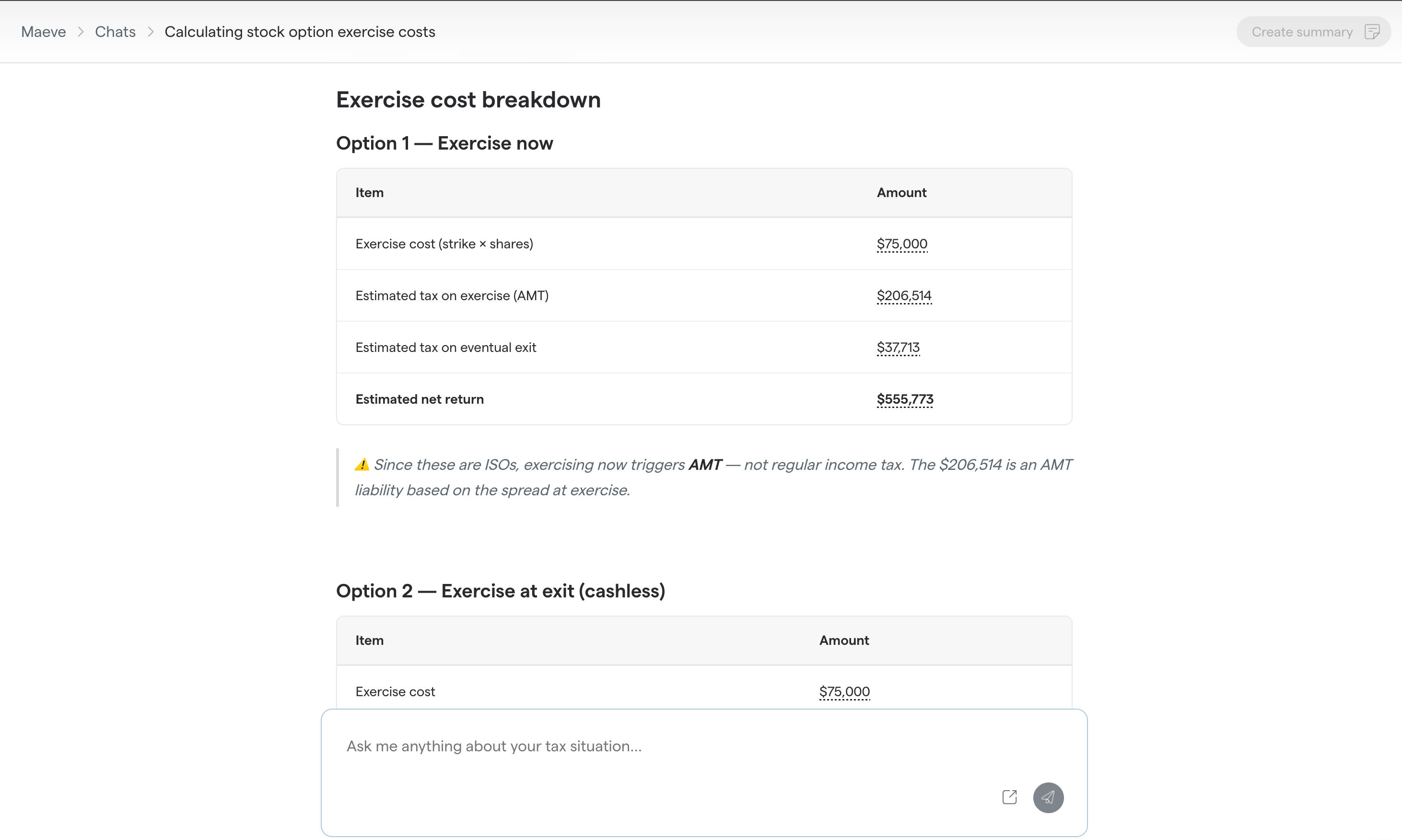

For example, you can compare what happens if you exercise now versus later, how changes in valuation affect your tax bill, or how different strategies could impact how much cash you keep.

Here’s an example for someone calculating their returns from exercising now vs an exercise at exit.

For illustrative purposes only. Actual results may vary and there is no guarantee of any particular outcome.

One of the biggest barriers to acting on equity is the upfront cost, both the exercise price and the taxes that can come with it. This can make even well-timed decisions feel out of reach.

Secfi offers non-recourse financing designed specifically for pre-IPO equity, enabling you to exercise without using your own capital. Repayment is tied to a future IPO or acquisition, rather than requiring fixed payments regardless of outcome.

This makes it possible to act earlier, reduce personal financial risk, and avoid taking on traditional debt.

Non-recourse financing can work to your advantage if you:

Learn more about getting financing with us: Secfi’s non-recourse financing

It’s likely you’ve already worked with a tax advisor, financial planner, or investment manager. The challenge is that pre-IPO equity comes with scenarios that many traditional advisors don’t handle regularly, especially around exercising, taxes, liquidity timing, and concentration risk.

Working with someone who understands equity compensation can help you evaluate different paths with more accuracy, instead of trying to piece together complicated advice from different sources. This is especially valuable when you’re making decisions that could impact your taxes and long-term financial plans for years to come.

Beyond equity planning, many executives also want support connecting those decisions to their broader financial goals, whether that’s buying a home, planning for children, diversifying over time, or building long-term wealth after a liquidity event.

Secfi combines equity planning, financial planning, and wealth management designed specifically for tech professionals, helping you navigate complex equity decisions with guidance tailored to your situation.

Dan Sinner spent nearly a decade at Happy Money, holding roles including Marketing Director, VP of Growth, and Chief Customer Officer. He was part of the team that helped grow the company to a valuation of over $500 million.

With that level of experience, you might expect equity decisions to feel straightforward. But when it came time to make decisions about his own stock options, that wasn’t the case.

“Even as an executive, we're supposed to know all the things about all the things, which is not necessarily true,” Dan said. “Especially when it comes down to the complexity of taxes and different types of equity.”

The biggest challenge was the cost. Exercising his options meant using cash he wanted to spend on a home. Dan describes himself as relatively risk-averse when it comes to his own finances, despite working at a high growth startup.

At the same time, he was approaching an expiration deadline, which meant waiting indefinitely didn’t make sense anymore.

That’s when Dan began working with Secfi. He decided to use non-recourse funding, and was so pleased with the experience he decided his employees would benefit as well.

As a result, Happy Money partnered with Secfi to offer both education and financing options across the company. Dan said it felt better to point employees toward a trusted resource, rather than leaving them to piece things together on their own.

Read the full case study: Why a Happy Money executive introduced Secfi to the whole company.

Testimonials are specific to an individual Client’s experience and may not be representative of all Clients. Unless otherwise indicated, Clients offering a Testimonial do not receive compensation and their statement does not present a conflict of interest.

There’s no single “right” answer when it comes to your executive stock options, but we believe there are more thoughtful ways to approach the decision.

Without a clear framework, it’s easy to delay decisions or default to waiting for an exit, even when that may not be the most effective strategy.

The key is understanding your options, the tradeoffs involved, and how those decisions fit into your overall finances.

If you want to explore your options in more detail, you can start by modeling your equity with Maeve, our secure AI tool designed for the nuances of equity compensation. Or, if you’d prefer to speak with someone directly, you can reach out to our team.

The tool shown here uses artificial intelligence and is for illustrative purposes only and not necessarily indicative of future results and there is no guarantee that similar results can be achieved. The information provided by the tool is not professional advice and is not intended by Secfi, Inc., its affiliates, and Secfi representatives, to be deemed as investment, legal, tax or other professional advice or recommendations of any kind, or to form the basis of any decision to do or to refrain from doing anything. Secfi does not review the accuracy or completeness of the information provided to us within the tool.

There’s no one-size-fits-all answer, because the right timing depends on your company, financial situation, tax exposure, and risk tolerance. In some cases, exercising earlier can lower your taxes and increase long-term upside if your company’s value grows over time. In other situations, waiting may reduce risk if there’s uncertainty around the company’s future.

Many executives evaluate factors like exercise cost, taxes, liquidity timelines, and how much of their net worth is already tied to the company before making a decision. AI tools like Secfi’s Maeve can help model different scenarios so you can compare the tradeoffs more clearly.

The amount depends on your strike price, the number of options you want to exercise, and any taxes triggered by the transaction. For executives with large grants, the upfront cost can sometimes reach hundreds of thousands or even millions of dollars.

That’s why many executives don’t exercise all of their options at once. Instead, they may spread exercises across multiple years, exercise selectively, or explore alternatives like non-recourse financing to reduce the amount of upfront personal cash required. Companies like Secfi are purpose-built for providing non-recourse financing in these cases.

Exercising stock options early can sometimes reduce your long-term tax burden, especially if your company’s valuation increases later. It may also start the clock for long-term capital gains treatment.

However, exercising can also trigger taxes before you’ve received any liquidity from your shares. In some cases, executives may owe large tax bills even though they still can’t sell the stock. The exact impact depends on factors like the type of options you hold, how long you keep the shares, your income, and your company’s valuation. In addition, if your company does not exist, there could be additional tax consequences. It is always recommended that you speak to a tax professional regarding your circumstance.

Because the stakes can be high, many executives work with advisors or planning tools at companies like Secfi that specialize in equity compensation to model different tax scenarios before making a decision.

Non-recourse financing is designed to help employees and executives exercise stock options without using large amounts of personal cash upfront. Instead of requiring traditional loan payments or personal collateral, repayment is typically tied to a future liquidity event, such as an IPO or acquisition.

With Secfi’s non-recourse financing, executives may be able to cover both exercise costs and associated taxes while reducing personal financial risk. If there’s a successful exit, repayment comes from the proceeds. Because the financing is non-recourse, personal assets are generally not at risk if the company underperforms.

That depends on your goals, timeline, and comfort with risk. Holding your shares may maximize potential upside if your company continues to grow, but it can also leave a large percentage of your net worth tied to a single company.

Some executives choose to diversify over time so they’re not relying entirely on one outcome. Others prioritize long-term upside and continue holding most of their shares. In practice, many people land somewhere in between, balancing future growth potential with personal financial goals like buying a home, supporting family, or reducing concentration risk.

The important thing is making a deliberate decision based on your broader financial picture, rather than defaulting to “wait and see.” Financial modeling tools such as Maeve AI and equity specialists from companies like Secfi can help you put together a strategy that meets your financial goals.