Should you get a loan to exercise your startup stock options?

8 min

0 result

Mike’s a CPF® at Secfi. He specializes in helping clients make the most of their stock options and integrate equity compensation into their broader financial plans.

If you’re at a company whose valuation keeps going up, it’s likely that the cost of exercising your stock options is way more than you expected.

This is especially true for senior employees and executives at later-stage startups, where exercising stock options can require a significant amount of capital long before there's an opportunity to sell shares.

One question that often comes up in this situation is: Should you take out a loan to exercise stock options?

While loans are an option for getting the cash you need to exercise your stock options, they can carry a lot of personal risk and might not be enough to cover your entire exercise cost.

Ultimately, it comes down to your personal financial situation and risk tolerance.

Rather than a loan, you can also consider non-recourse financing. It looks a lot like a loan, but with some key differences. With non-recourse financing, your personal assets are not on the line.

So, if available to you (which depends on the company you have stock options in), non-recourse financing can cover the costs of exercising (including taxes) without the risk of losing your personal money – or even other assets – should things go wrong.

Here’s what we’ll cover:

Curious to learn more about how non-recourse financing could help you? See if you qualify by signing up and requesting financing: Get Started

A personal or consumer loan is any kind of loan that you can get straight from a bank or consumer-lending startup.

While you could potentially get some capital this way, consumer loans typically top out at $50,000. That won’t do you much good if you’ve got exercise costs of $200,000 or more.

And personal loans can come with very high interest rates, some can be in the neighborhood of 20% or higher. At that rate, you’d end up paying over $26,000 in interest for a $50,000 loan over a 5-year period. And you’ll have monthly payments due immediately — even though you don’t know when you’ll be able to sell your shares.

And if the value of your shares tank or your company never exits, you still have to pay back the loan balance.

If you’re a homeowner, then home equity loans are another possibility.

Because your home is used as collateral, you can get better interest rates and larger borrowing amounts.

That’s great, but the major drawback is that your house is on the line.

If things go south for your company for any reason and your shares become worthless, you’ll still be responsible for making these payments until the loan is paid off.

A margin loan — also known as a portfolio line of credit — allows you to borrow against a portfolio of stocks you've been investing in.

Similar to a home equity loan, you can get more favorable interest rates when taking out a margin loan.

If the market is high, it’s a favorable time to take out one of these loans.

But if you take out a loan and then the value of your portfolio drops, your lender may ask you to put up more money or assets to collateralize the loan.

If the point of getting the loan in the first place is you don't have any cash available, then this will be an issue. And since it’s a full-recourse loan, your personal assets are at stake if you can’t pay it back.

For executives, margin loans can create a double concentration problem. You're borrowing against one investment portfolio in order to increase your exposure to another concentrated position: your company stock. If public markets decline while your startup's prospects weaken, you may face pressure on both sides of your balance sheet at the same time.

While it’s pretty uncommon, some startups will provide their employees with a private company loan to exercise stock options.

For this to happen, employees sign a promissory note stating they will pay their company the required exercise amount in the future and then the employee uses that promissory note to pay for the exercise price of their options as well as taxes (although this depends on the situation).

You only pay the loan back once you sell your shares. No monthly payments due.

It may seem like a great option if you can’t afford to exercise, but it comes with a catch: if for any reason your company fails, its creditors will effectively own all the company’s assets—including any outstanding debts (like your loan).

In that case, your shares would be worthless and you could have creditors wanting your loan repaid in full—regardless of what you’d have to sell to pay it.

This can be especially relevant for executives who leave a company before an IPO and suddenly face a large post-termination exercise decision. Preserving ownership may require significant capital at exactly the moment compensation from the company is ending.

By the way, be careful when taking a loan from your employer. If the terms are too preferential and look like a non-recourse loan, the IRS could consider it disguised compensation, triggering taxable income or making your exercise invalid.

If you don’t have enough money to self-fund the exercise of your stock options and loans are too risky, your next best financing option could be non-recourse financing.

Non-recourse financing is a cash advance that covers the cost of exercising plus any tax burden that exercising incurs. It sounds like a loan, but it’s different. For starters, there are no monthly repayments. You only pay the amount back after there’s been a successful exit and you sell your shares.

But the most important difference: if in a bad scenario there’s no exit, you don’t have to pay back the loan balance.

That’s why it’s called non-recourse: your shares securer the amount financed. Apart from the shares, none of your personal assets are on the line.

This can be particularly relevant for executives facing seven-figure exercise costs or significant AMT obligations. Rather than liquidating other investments, taking on recourse debt, or further concentrating personal financial risk, some executives use non-recourse financing to preserve flexibility while maintaining ownership of their equity.

At Secfi, we offer non-recourse financing to startup employees and executives If your company goes downhill or never exits, we take the hit. If your company doesn’t go public, there may be additional tax consequences depending on your particular circumstance so it is always important to speak to a tax professional.

We often get the question how we can afford to take all the risk. It’s because:

We don't have any maximum or minimum requirements, so we’re able to cover the cost of exercising, whether you need $100,000 or $10 million.

One option that a lot of employees have taken is to simply wait until an IPO happens and then do what’s called a cashless exercise.

That’s basically where you exercise and sell your options on the same day to cover the costs. This way you avoid the upfront need for cash.

The drawback is that you may end up paying significantly more in taxes. That’s because if you exercise your options and hold the shares for at least a year before selling them (and meet the other applicable holding requirements), you may qualify for long-term capital gains treatment rather than being taxed at higher short-term rates.

Depending on your income and state of residence, the difference can be substantial. In some cases, the potential tax savings can amount to as much as 27% of the gain.

The more successful your company ends up becoming, the more this matters. We’ve seen cases of very successful IPOs where the average employee paid an extra million bucks in taxes (like DoorDash).

The other drawback is for many companies you’ve got to still be at your company when the IPO happens in order to do a cashless exercise .

You can’t leave and do anything else with your career if you’ve got a sizable amount of unexercised options and you’re waiting for a cashless exercise. Because if you do leave, you usually get just 90 days to exercise before your options expire. This is often referred to as golden handcuffs.

Having said that, some companies do offer extensions (although you lose out on the preferential tax treatment of your incentive stock options (ISOs), because they convert to non-qualified stock options (NSOs)).

For some employees, selling stock options on a secondary market is also possible.

By selling some of your shares, you can generate cash to help cover the costs of exercising the rest. Not every company allows secondary sales, and even when they do, finding a buyer isn't always straightforward. Demand for private-company shares can vary significantly depending on the company, market conditions, and investor interest.

Even if you do find a buyer, there are some downsides to consider. The biggest is that if you sell and your company's value continues to rise before a successful IPO or acquisition, you miss out on those future gains.

It's also common for buyers in the secondary market to purchase shares at a discount to the company's most recent valuation. That means you may end up receiving less for your shares than you expected.

Another consideration is taxes. For the portion you sell, your proceeds may be taxed at relatively high rates depending on your holding period, the type of equity you own, and your overall tax situation.

Executives are also more likely to face significant AMT bills when exercising ISOs, making the tax cost as important as the exercise cost itself.

Secfi helps startup employees and executives navigate the complexity of stock options with planning tools, expert guidance, and non-recourse financing solutions.

We founded Secfi after experiencing the problem firsthand: the cost of exercising stock options — and the taxes that come with them — can be too high for many employees to afford on their own. We built Secfi to help tech employees access the upside of their equity without taking on unnecessary personal financial risk.

We've worked with employees across every level of startup organizations, from early hires to C-suite executives navigating complex equity and tax decisions.

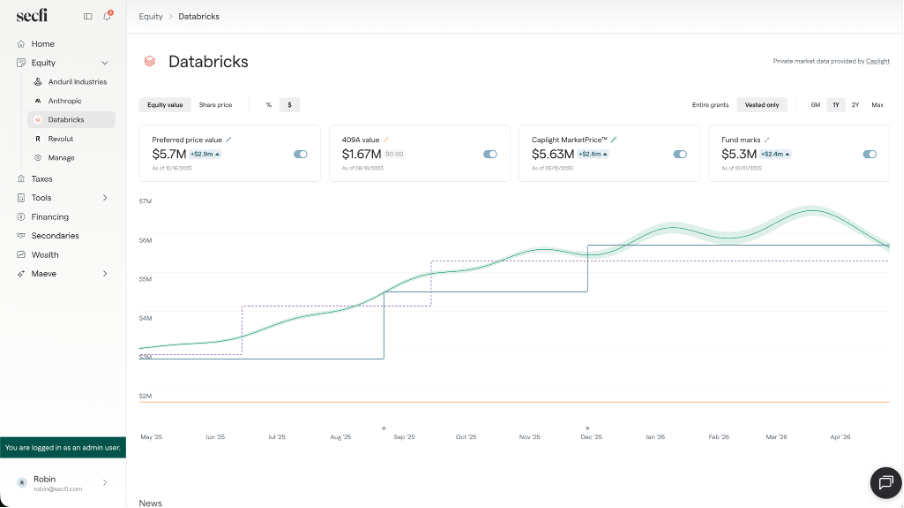

Today, employees at companies like Databricks, Anduril, and Gusto work with Secfi to better understand their equity, plan their strategy, and access financing that lets them exercise stock options without putting their personal assets on the line.

As we’ve mentioned above, if the upfront cost of exercising your stock options feels out of reach, non-recourse financing can give you another path forward.

Secfi is one of the leading financing partners focused specifically on startup employees and tech executives. We help employees access the cash they need to exercise their stock options and cover related taxes — without taking on the same level of personal risk as a traditional loan.

Unlike personal loans or margin loans, Secfi’s financing is non-recourse. That means your personal assets are not on the line. If your company never exits or your shares ultimately become worthless, you don’t owe anything back personally. If your company does have a successful IPO or acquisition, Secfi gets repaid from the proceeds and takes a portion of the upside.

Secfi can also help you explore selling your shares on the secondary market, allowing you to potentially sell some of your shares through our network of buyers. We handle the process from start to finish, including coordinating with buyers, navigating paperwork, and helping you understand the tax implications.

Exercising stock options is a tax, timing, and risk-management decision — and the right move depends heavily on your company, your equity package, and your long-term financial goals.

At Secfi, equity is what we do. Our team works with startup employees and executives every day to help them navigate complex equity decisions. Our Equity Strategists specialize in stock options, liquidity planning, and pre-IPO financial scenarios, and our broader wealth advisory team helps clients think through their full financial picture.

That means we can help you go beyond simply accessing financing. We can also help you answer questions like:

There’s no one-size-fits-all answer. The right strategy depends on your goals, risk tolerance, timeline, and company outlook.

Our role is to help you understand your options clearly so you can make a more informed decision about what makes the most sense for your situation.

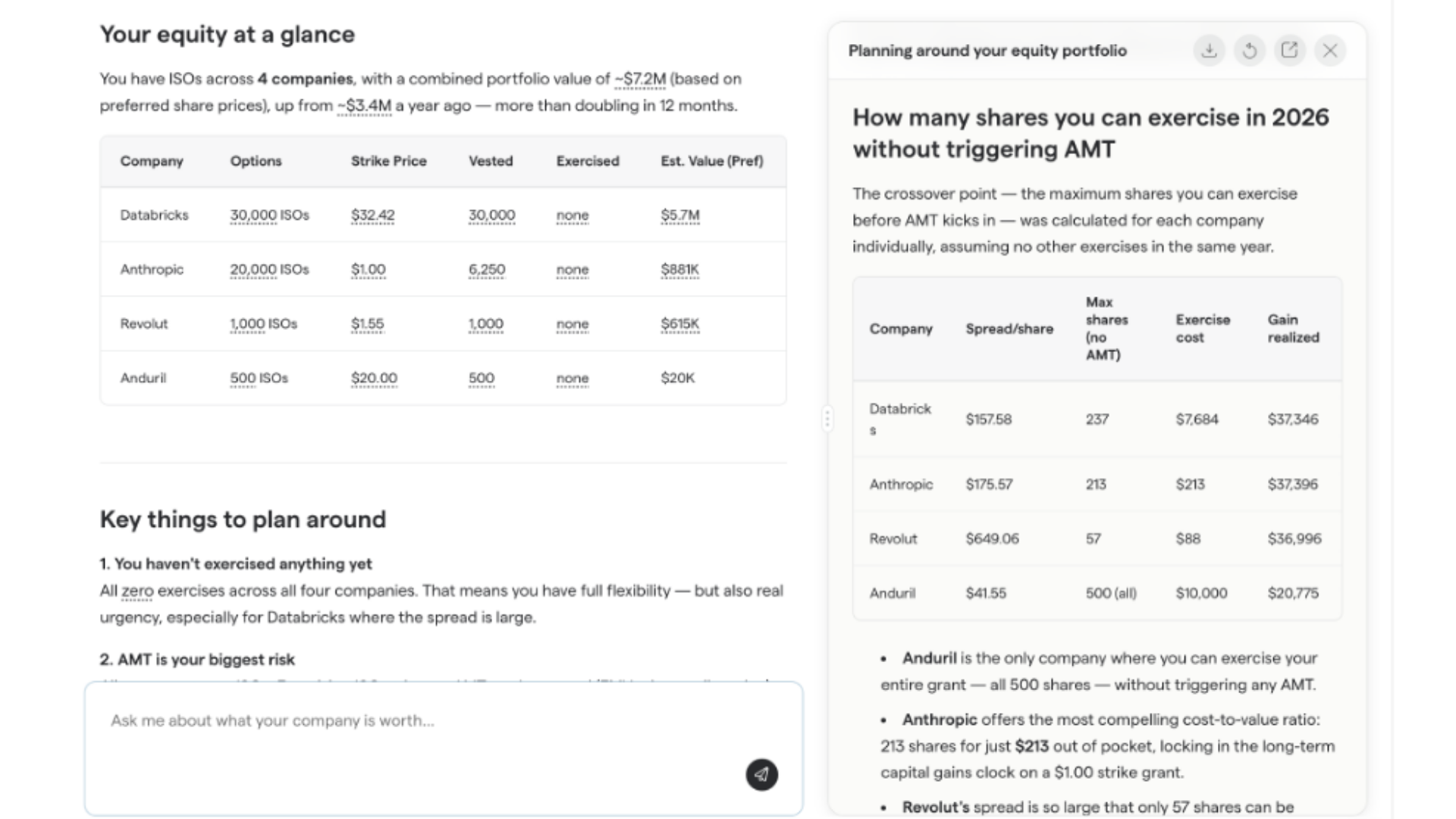

One of the biggest challenges with employee stock options is understanding the tradeoffs between different choices before you commit to one.

Should you exercise now or wait? How much could AMT cost you? What happens if your company’s valuation increases before an IPO? Would financing help preserve liquidity, or would selling shares on the secondary market make more sense?

Here’s where Secfi can help: We’re one of the only platforms that combines equity planning tools, private market insights, and non-recourse financing in one place. Instead of relying on rough spreadsheets or generic online calculators, you can use Secfi’s platform to compare different strategies based on your actual equity information.

For illustrative purposes only. Actual results may vary and there is no guarantee of any particular outcome.

You can also use Maeve, Secfi’s AI equity strategist, to explore different scenarios and better understand the financial implications of your choices.

Unlike general AI tools, Maeve is purpose-built for equity planning and runs on top of Secfi’s proprietary calculation engine. That means it’s designed specifically for the types of questions startup employees and executives face, not general financial advice or broad internet knowledge.

Maeve can help you analyze scenarios related to:

The tool shown here uses artificial intelligence and is for illustrative purposes only and not necessarily indicative of future results and there is no guarantee that similar results can be achieved. The information provided by the tool is not professional advice and is not intended by Secfi, Inc., its affiliates, and Secfi representatives, to be deemed as investment, legal, tax or other professional advice or recommendations of any kind, or to form the basis of any decision to do or to refrain from doing anything. Secfi does not review the accuracy or completeness of the information provided to us within the tool.

Maeve also has access to private market valuation data and broader market context, helping you evaluate your equity decisions with more accurate and specialized information than you’d typically get from a general-purpose AI tool.

With Maeve you can more easily understand the pros, cons, risks, and tradeoffs of each path so you can make a more informed decision about your equity.

When a former Confluent employee decided to leave the company, he faced a common startup dilemma: he only had 90 days to exercise his stock options before losing them.

Once he calculated the exercise costs and potential tax bill, he realized the financial risk was significant. While he believed in Confluent’s future, he wasn’t comfortable risking a large amount of personal savings without knowing when — or if — the company would IPO.

“That was the big gamble,” he said. “I had the funds that I could have used for the exercise. But it was that whole tax liability at the end of the year.”

After hearing about Secfi from a coworker, he researched several equity financing providers before making a decision. What stood out was Secfi’s transparency and consultative approach.

“Secfi was very upfront,” he said. “One of the things I really appreciated was the fact that they talked through that whole scenario.”

Rather than pushing him toward financing, the team answered his questions, walked through different outcomes, and encouraged him to compare alternatives.

“I'd actually talked to a couple of different companies that handle these kinds of transactions,” he said. “And Secfi was the most attractive.”

Not long after, Confluent went public. Today, he owns shares in a public company and says he has no regrets about the decision.

Read case study: Barry chose Secfi’s equity financing because of the people, transparency, and reduced risk to own his options

Testimonials are specific to an individual Client’s experience and may not be representative of all Clients. Unless otherwise indicated, Clients offering a Testimonial do not receive compensation and their statement does not present a conflict of interest.

Exercising your stock options is often too expensive to pay for by yourself – but taking out a loan can be risky (and may not cover your entire costs, especially if you factor in taxes).

Non-recourse financing can be a good alternative. It looks like a loan, but it’s specifically intended for the purpose of exercising startup stock options.

You’ll only pay the financing back after the startup has exited – and if for some reason that never happens, you won’t have to pay it back at all. Your personal savings are always left untouched.

The tool shown here uses artificial intelligence and is for illustrative purposes only and not necessarily indicative of future results and there is no guarantee that similar results can be achieved. The information provided by the tool is not professional advice and is not intended by Secfi, Inc., its affiliates, and Secfi representatives, to be deemed as investment, legal, tax or other professional advice or recommendations of any kind, or to form the basis of any decision to do or to refrain from doing anything. Secfi does not review the accuracy or completeness of the information provided to us within the tool.

Traditional loans can expose your personal finances to significant risk. You may still owe monthly payments, interest, or the full loan balance even if your startup’s shares lose value or become worthless. Certain loans, such as home equity or margin loans, can also put your house or investment portfolio at risk.

Waiting for an IPO and doing a cashless exercise can reduce upfront cash needs because you exercise and sell shares simultaneously. However, this strategy may result in significantly higher taxes because you may not qualify for long-term capital gains treatment. It can also create “golden handcuffs,” since employees often need to remain at the company until the liquidity event occurs.

The right strategy depends on factors like your company’s growth prospects, your personal risk tolerance, tax exposure, liquidity needs, and long-term financial goals. Many employees model different scenarios — including AMT exposure, capital gains taxes, and potential future valuations — before deciding whether to exercise using personal cash, financing, or secondary sales.