How are stock options taxed? What employees need to know before exercising

17 min

0 result

San Francisco native (yes, really). @uw and Lowell High alum. I like to nerd out on fintech, stock options and taxes.

If you’re a startup employee earning stock options, it’s important to understand how your stock options are taxed. If your eyes just glazed over, we get it — taxes aren’t fun.

When you understand how stock option taxes work, you can take steps to help reduce your tax liability, and potentially make more money when it’s time to sell your shares. And we’re not talking about the difference of a few extra dollars. Being smart about your stock option taxes may translate into a more than 20% net gain after your startup exits.

Unfortunately, there's often a big knowledge gap in this area. Many startup employees aren't even aware they need to pay taxes when they exercise their stock options, or that the tax implications can hit years before they ever see a dollar of liquidity.

We’re here to help. In this guide, we cover:

Note: looking to model out how much you’ll pay in taxes if you exercise stock options? Try our AI equity assistant, Maeve, which is specifically designed for equity calculations for free: Get started now.

There are two times you’ll likely owe taxes — both federal and state — with stock options:

Your taxes at exercise depend on the type of stock options you’re earning because Incentive Stock Options (ISOs) and Non-qualified Stock Options (NSOs) are taxed differently.

In the U.S., ISOs are taxed under the alternative minimum tax (AMT) system.

Most people are familiar with the regular income tax system — it’s what applies to your salary and bonuses. But there’s also a parallel tax system, the AMT, which can apply in certain situations, including when you exercise ISOs.

When you exercise ISOs, the IRS treats the difference between your exercise price and the company's current share value as income for AMT purposes, even if you haven't sold the shares yet or made any cash. If that “paper gain” is large enough, you may owe AMT when you file your taxes.

For example, imagine your strike price is $2 per share, and the company's latest 409A valuation — the fair market value (FMV) the company uses for tax purposes — is $20 per share. Exercising 10,000 options would create a $180,000 paper gain in the eyes of the IRS, and that amount could trigger AMT.

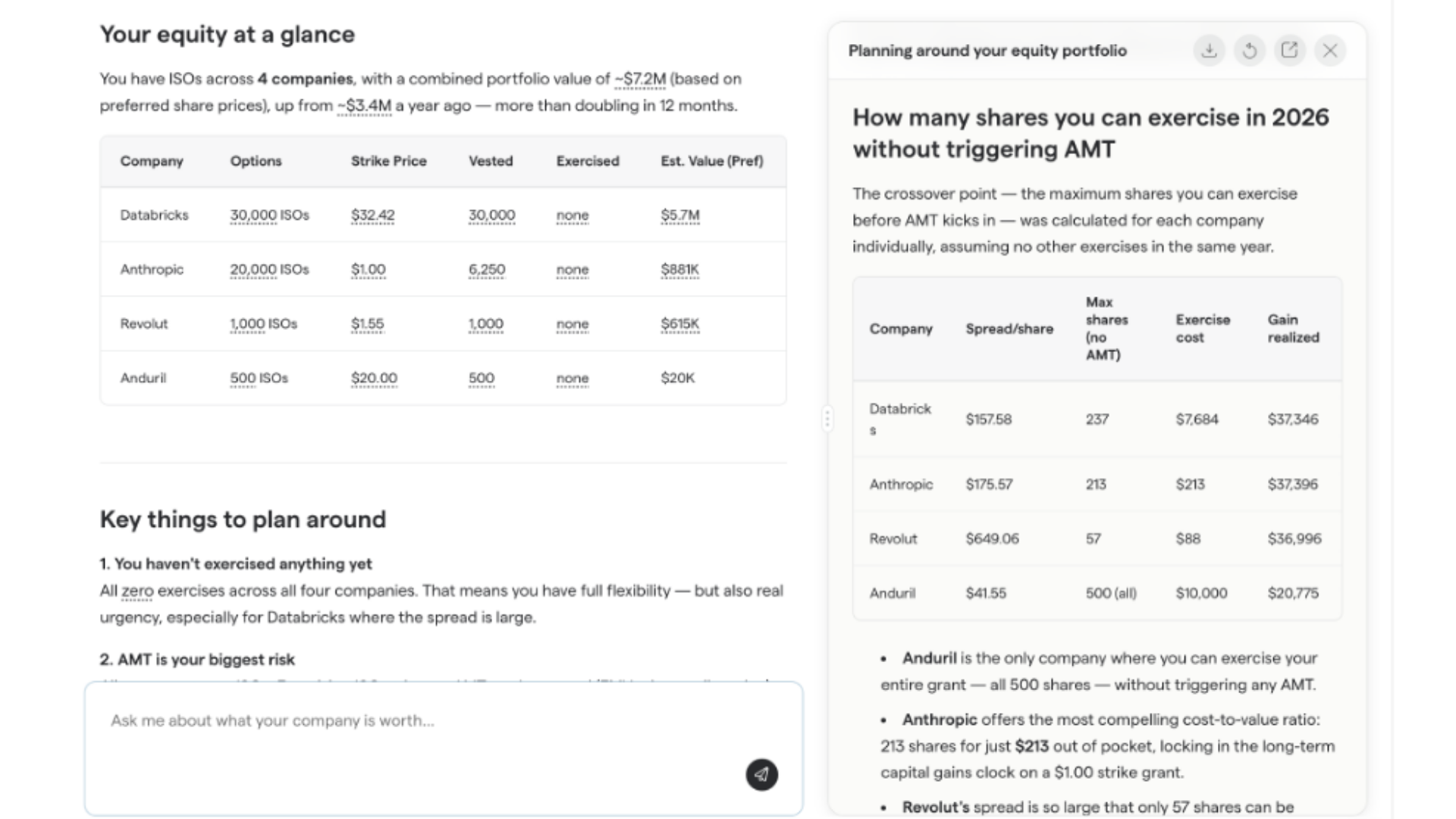

The good news is that AMT isn’t all-or-nothing. Many employees choose to exercise only enough ISOs each year to stay below the AMT threshold. By spreading exercises over multiple years, they may be able to start the clock on long-term capital gains treatment without creating a large upfront tax bill. If you're unsure how much you can exercise before triggering AMT, Maeve — Secfi's AI equity assistant — can help you model different exercise scenarios, estimate your tax exposure, and understand the potential tradeoffs before making a decision.

If you have NSOs, you'll generally owe ordinary income tax when you exercise them, based on the difference between your strike price and the shares' fair market value. Keep in mind that exercising NSOs could push you into a higher tax bracket.

When you later sell the shares, any additional gain is typically taxed as either a short-term or long-term capital gain, depending on how long you've held the shares.

With both ISOs and NSOs, your tax obligation at exercise is based on the difference between your strike price — the fixed price at which you can buy your company stock — and how much the shares are worth, set by the company's most current fair market valuation (also known as a 409A valuation), or the company's public market price.

When you exercise ISOs or NSOs, you’re buying shares in the company. Tax authorities consider these shares to have value, based on the company’s 409A valuation on the day you exercise. That value exists, even though most pre-IPO shares are illiquid, meaning no buyers exist for the shares, because the shares are not publicly traded.

If the company’s 409A valuation is higher than your strike price, you’re making a “paper gain” in the eyes of the IRS. You’re then taxed on that assumed gain.

This tax structure has an important implication: If your company keeps growing, then exercising your employee stock options becomes more expensive over time. The higher the 409A valuation, the larger your assumed gain, and the more tax you’ll owe.

When you sell shares, your tax bill is largely influenced by how long you’ve held the shares. When you sell shares for more than you paid for them, you’ve created a capital gain. The federal government and many states have specific tax systems for the income generated by capital gains.

Capital gains are either long-term or short-term, based on the amount of time between when you exercised the stock options and when you sold the shares — also known as your holding period.

To qualify for long-term capital gains on ISOs, you'll need to meet the holding period requirements: hold the shares for at least two years after the grant date, and at least one year after you exercised them.

It’s a little easier when selling NSOs — you’ll just need to hold onto your NSOs for at least one year after exercising them to qualify for the long-term capital gains rate.

Tax rates for long-term capital gains can be significantly lower than the rates applied to short-term capital gains. Federal long-term capital gains rates range from 0% to 20%, depending on how much money you earn in the sale, and the other income you earned that year.

Meanwhile, short-term capital gains are taxed according to your income tax bracket, which can be as high as 37% at the federal level.

Individual states tax capital gains differently. For example, in California and New York, the tax authorities there make no distinction between long-term and short-term capital gains, and tax all capital gains as ordinary income.

A few states, like Florida and Texas, don’t collect state income taxes, or taxes on capital gains.

It’s worth noting that short-term capital gains on employee stock options could be taxed at a higher rate than your regular income, because the sale of those stock options could push a portion of your income into a higher tax bracket.

Incentive stock options are a type of stock option popular with pre-IPO startups, because they enjoy more favorable tax treatment than other types of stock options.

ISOs are often (and incorrectly) touted as tax-free at exercise. That's not necessarily true — depending on the number of shares you're exercising, your exercise price, and the company's current 409A valuation, you could potentially owe thousands of dollars, or more, at exercise.

Most people aren’t familiar with AMT, so it can be a major source of confusion when they go to exercise their stock options and realize they didn’t plan for the AMT, which drives up their cost of exercising significantly.

The AMT is a parallel tax system in the U.S. meant as a fallback to prevent excessive tax avoidance. It builds up in parallel to your income tax liability, according to a different ruleset.

If you exercise enough ISOs in a single year, you could trigger AMT. People owe AMT on top of their typical income taxes. How much you’ll owe in AMT involves a complicated calculation based on your income, the AMT exemption, and the assumed value of your exercised stock options.

In later years, you can get back what you pay in AMT in the form of the AMT credit. The federal government, and several states — notably, California — have an alternative minimum tax. Every year that you file your tax return, you’re required to calculate your income tax liability as well as your AMT.

You can read a full guide on AMT here: What is the alternative minimum tax (AMT) and how does it work?

How much you’ll owe in AMT is based on the difference between your employee stock option’s strike price (how much you pay to buy shares) and the 409A valuation (how much the shares are valued at upon exercise).

Note: With ISOs, there is a tax-free threshold, so you only owe taxes beyond the threshold.

Let’s consider an example. You’re a tech worker in California, earning a six-figure salary at a pre-IPO startup:

In this example, exercising your shares could trigger a significant AMT bill. A common mistake is to estimate AMT using a simple percentage of the paper gain, but the actual calculation depends on factors like your income, filing status, deductions, state taxes, and any prior AMT credits.

As a rough illustration, your total out-of-pocket cost could be substantially higher than the $45,000 exercise cost alone once taxes are factored in. However, the actual amount varies widely from person to person.

To estimate your specific AMT exposure, use Secfi's free AI equity assistant, Maeve. Maeve uses your equity details and tax information to model the actual calculation rather than relying on a back-of-the-envelope estimate. Because AMT rules are complex, you should also consider speaking with a qualified tax advisor before making an exercise decision.

AMT surprises most people because it’s not automatically taken out or calculated when stock options are exercised. Then, when they go to file their taxes they learn they have an unforeseen cost.

Note that your company will not handle any taxes for you when you exercise ISOs, and that it’s up to you to pay and report any taxes you owe. You’re only paying your company the base cost of exercising options.

After exercising ISOs, you should receive IRS Form 3921 from your employer. This form will include important dates and values needed to properly report taxes when you eventually sell the shares.

You and/or your tax professional will use IRS Form 6251 to determine if you’re subject to the federal AMT and calculate associated taxes.

When it’s time to sell your ISOs, there can be significant tax savings if you qualify for long-term capital gains, versus short-term capital gains.

Let’s build on the example above — remember, in this example, you’re a tech worker in California, earning a six-figure salary at a pre-IPO startup:

If you’ve held your shares for less than a year, you’ll owe an estimated short-term capital gains tax of $831,250. If you hold your shares for more than a year (and more than two years after the ISOs were initially granted), you’ll owe long-term capital gains tax of $500,500.

Depending on your specific numbers, you could end up saving thousands of dollars (and in some cases, hundreds of thousands of dollars) by taking advantage of long-term capital gains. Check out Secfi’s free AI equity assistant Maeve to begin to build an estimate of your stock option tax liability.

When you sell your shares, you’ll receive an IRS Form 1099-B from the brokerage firm that handled the stock sale. This form reports any capital gains or losses resulting from the transaction, which you’ll use to report on Schedule D of your IRS Form 1040.

If you’re earning ISOs, there are three main strategies to minimize your tax liability: Exercising your ISOs early, exercising a small number of ISOs each year, and performing a cashless exercise.

Some startups allow employees to exercise some or all of their ISOs before they vest, a strategy known as “early exercise.” Because early-stage companies often have very low fair market values, early exercising can allow employees to buy shares while the spread between the strike price and fair market value is small, potentially reducing or eliminating AMT. You can still exercise after the options are vested as well when the 409A is still lower.

Separately, shares in some early-stage startups may qualify for Qualified Small Business Stock (QSBS) treatment. QSBS is a special tax exemption that can allow eligible shareholders to exclude up to millions of dollars in gains from federal taxes if they meet certain requirements, including holding the shares for at least five years.

The major risk of early exercise is that the value of your shares could decline, or collapse entirely, while you’re waiting to sell your ISOs. Exercising pre-IPO shares is inherently riskier than waiting until an exit to exercise.

Startup employees earning ISOs can always decide to exercise (i.e., purchase) just enough ISOs each year to remain under the AMT threshold. This strategy works best when an ISO’s strike price and 409A valuation is still relatively near one another in value. If you’d like to explore this strategy, check out Secfi’s free AI equity assistant, Maeve, to calculate your AMT.

Cashless exercises are the most common strategy that people use with ISOs, because many can’t afford to exercise before an exit event. Cashless exercises require no upfront cash, and as a result, carry the least amount of risk — you’re able to see exactly how much it will cost to exercise your ISOs, and the exit price.

In a cashless exercise, you sell some or all of your shares, and then use the resulting funds to cover any exercise costs and associated taxes, in what the IRS effectively treats as a single transaction.

There are two major drawbacks to a cashless exercise: One, you’ll pay ordinary income tax on any gains, and two, you may need to stay employed until the exit event occurs, which could be many years in the future. On top of that, you will need your company to allow you to perform a cashless exercise which includes potentially finding a buyer for your shares.

Non-qualified stock options (NSOs) don’t enjoy the same preferential tax treatment that ISOs do. At startups, they’re typically issued to contractors, vendors, and executives.

In some cases, they’re granted to former employees who leave the company, and fail to exercise their ISOs inside the company’s 90-day post-termination stock option exercise window. In those cases, unexercised ISOs get automatically converted into NSOs.

Like ISOs, NSOs are taxed when you exercise them, and when you eventually sell them.

How much you’ll owe in taxes at exercise is based on the difference between your stock option’s strike price (how much you pay to buy shares) and the company’s 409A valuation (how much the shares are valued at upon exercise).

For example, you’re a tech worker in California, earning six figures at a pre-IPO startup:

NSOs are taxed at ordinary income tax rates, so in this example, you’d pay around 46% in combined California state taxes and federal taxes — roughly $221,000. Note: Your tax rate at exercise is affected by your other income.

That means exercising your NSOs would cost $266,000 ($45,000 to purchase the shares, and $221,000 in taxes). If you’d like to calculate your NSO taxes, use Secfi’s free AI equity assistant, Maeve.

Exercising NSOs triggers a tax withholding requirement at your company — just like if they were paying out a cash bonus. The company collects payment from you to submit taxes to the government on your behalf.

When you exercise NSOs, your company will send you an estimate of the withholding tax that they are required to send to the government. You’ll need to pay the company your exercise costs, as well as the estimated tax withholding, to exercise your NSOs.

Note: Companies are only legally required to withhold the minimum amount of taxes when you exercise NSOs. You’ll want to double-check that amount with the help of a tax professional, to make sure you don’t inadvertently owe a surprise tax bill when it comes time to file.

When you file your tax return, you’ll calculate your actual tax bill against what your company withheld. If your withholding is greater than your actual tax bill, you’ll get a return of cash due to overpayment. If your withholding is smaller than your actual tax bill, you’ll owe additional taxes.

Ultimately, it’s your responsibility to pay the correct amount of taxes when you exercise your NSOs. You could be required to make estimated tax payments throughout the year to supplement your employer’s withholding. Make sure you’re paying your taxes on time to avoid future penalties.

As we covered earlier, you’ll owe taxes when you exercise (i.e., purchase) your NSOs, and you’ll owe additional taxes if the shares continue to grow in value, and you eventually sell them at a profit.

When you sell your NSOs, you create either a capital gain or a capital loss, depending on whether your sale price comes in above or below your cost basis.

If you experience a capital gain, you’ll owe taxes based on how long you’ve held the shares — long-term capital gains if you’ve held the shares for at least one year after exercising them, or short-term capital gains if you’ve held the shares for less than a year.

Note: States tax capital gains at different rates. For example, in California and New York, state tax authorities make no distinction between short-term capital gains and long-term capital gains — all capital gains are taxed as ordinary income. Other states, like Texas and Florida, do not tax capital gains.

When you sell your shares, you’ll receive an IRS Form 1099-B from the brokerage firm that handled the stock sale. This form reports any capital gains or losses resulting from the transaction, which you’ll use to report on Schedule D of your IRS Form 1040.

There are two ways to minimize taxes when buying and selling NSOs: Exercising now to start the clock on long-term capital gains, and performing a cashless exercise to reduce upfront taxes.

If you’re earning NSOs and want to take advantage of the long-term capital gains tax rate, you’ll need to exercise your stock options to start the clock on that lower tax rate. To qualify, you’ll need to hold onto your exercised shares for at least one year before selling them.

The major risk is that the value of your shares could decline, or collapse entirely, while you’re waiting to sell your NSOs.

Most people who earn NSOs perform what’s known as a cashless exercise, where they sell some or all of their shares, and use the money to pay exercise costs, and any associated taxes.

The major benefits to a cashless exercise are twofold: One, you reduce your risk because you know how much your shares will cost, and how much they’re worth, and two, you don’t have to spend any upfront money of your own.

The drawbacks are also twofold: One, you’ll pay the highest possible combined tax rate on the transaction, lowering your total gains, and two, you’ll likely need to stay in your job until the exit to perform a cashless exercise.

At Secfi, we combine equity planning experience, specialized tools, and financing solutions to help startup employees navigate stock option taxes with more confidence.

If you feel confused by stock option taxes, you are not alone. Most people are never taught how equity compensation works, let alone how exercising options can create large tax bills years before there is any liquidity.

That knowledge gap is one of the reasons Secfi exists.

One of the best ways to reduce taxes is to model your scenarios before making a decision. That is exactly what Maeve was built for.

Maeve is Secfi’s AI equity assistant, designed specifically to help startup employees make more informed decisions. Connect your equity and tax information, and Maeve uses your actual data to model different outcomes based on your situation.

Unlike generic AI tools, Maeve is built on top of Secfi’s proprietary calculation engine and equity infrastructure. It is purpose-built for questions around ISOs, NSOs, AMT, exercising timing, capital gains, and private market equity planning.

That means you can explore questions like:

For illustrative purposes only. Actual results may vary and there is no guarantee of any particular outcome.

Maeve also has access to private market pricing data and equity-specific scenario tools, helping you understand not just the taxes involved, but also what your equity may be worth.

Rather than relying on generic outputs from tools like ChatGPT, you get calculations and insights built on your actual equity and tax situation.

Many people already have accountants, tax preparers, or financial advisors. But equity compensation is highly specialized, and many traditional advisors simply do not work with startup equity every day. At Secfi, this is our focus.

Our team works with startup employees and executives navigating stock options, AMT exposure, liquidity events, and concentrated equity positions every day.

By working with Secfi Wealth and our certified financial planners, you get a financial plan tailored to your goals, an approach that evolves with your situation, and a portfolio designed to complement your career and equity position.

One of the biggest challenges with stock options is that exercising them can become extremely expensive.

The average tech employee needs hundreds of thousands of dollars to exercise their options and cover taxes. Even employees with strong salaries often do not want to lock that much personal cash into a single illiquid company.

That is where non-recourse financing comes in. Secfi can provide the capital needed to exercise your options and cover associated taxes, while allowing you to retain ownership of your shares and avoid putting your personal assets at risk.

After assessing your company and equity situation, Secfi fronts the cash needed to exercise the options and pay taxes. Repayment only happens if there is a future liquidity event, such as an IPO or acquisition.

If the company never exits, you owe nothing. For many startup employees, this creates a way to participate in the upside of their equity without taking on the financial risk of writing a massive personal check upfront.

We have worked with employees from companies like Databricks, Gusto, and Anduril to help them exercise their options and navigate the associated tax costs.

You can learn more about non-recourse financing here: What is non-recourse financing for stock options?

Victor, an engineering leader at a pre-IPO startup, had modeled multiple exercise scenarios on his own. Each one seemed to create a different tradeoff between taxes, risk, and potential upside.

“I’m reasonably conservative. I try to keep my personal finances safe,” Victor explained. “Secfi felt like the safest option. There is upside, maybe a little less than the other possibility, but there is almost no downside.”

Victor had enough savings to exercise his ISOs himself, but once he calculated the potential AMT bill, the total cost became difficult to justify comfortably.

Buying the shares outright would have tied up a significant portion of his savings in a single illiquid company. Traditional loans also did not feel attractive because they could expose his personal assets to risk.

With Secfi’s non-recourse financing, Victor was able to exercise his stock options and cover the potential AMT bill without risking his personal assets. If the company successfully exited, Secfi would participate in the upside. If the company failed to exit, Victor would owe nothing.

For him, it created a way to participate in the company’s potential upside while keeping his personal financial risk manageable.

Read the full case study here: Why this engineering leader chose Secfi to finance his stock options

Testimonials are specific to an individual Client’s experience and may not be representative of all Clients. Unless otherwise indicated, Clients offering a Testimonial do not receive compensation and their statement does not present a conflict of interest.

There are many legitimate ways to reduce stock option taxes.

Some employees exercise smaller portions of their ISOs over multiple years to stay below the AMT threshold. Others exercise early to start the clock on long-term capital gains treatment. Some choose to wait for more clarity around a company’s valuation or liquidity timeline.

The challenge is that these decisions can involve hundreds of thousands of dollars, and small differences in timing can create dramatically different outcomes.

That is why it helps to work with tools and advisors built specifically for equity compensation planning.

Secfi helps startup employees model different exercise, tax, and liquidity scenarios so they can make more informed decisions about their equity and potentially reduce unnecessary taxes along the way.

The tool shown here uses artificial intelligence and is for illustrative purposes only and not necessarily indicative of future results and there is no guarantee that similar results can be achieved. The information provided by the tool is not professional advice and is not intended by Secfi, Inc., its affiliates, and Secfi representatives, to be deemed as investment, legal, tax or other professional advice or recommendations of any kind, or to form the basis of any decision to do or to refrain from doing anything. Secfi does not review the accuracy or completeness of the information provided to us within the tool.

Yes — in many cases, exercising stock options can trigger taxes even if you haven’t sold the shares yet. The tax treatment depends on whether you have ISOs (Incentive Stock Options) or NSOs (Non-Qualified Stock Options). ISOs can trigger alternative minimum tax (AMT), while NSOs are generally taxed as ordinary income at exercise.

ISOs and NSOs are taxed differently. ISOs may qualify for favorable long-term capital gains treatment if holding requirements are met, but they can trigger AMT at exercise. NSOs are taxed as ordinary income when exercised, based on the spread between the strike price and the company’s current fair market value. Any additional appreciation after exercise may then be taxed as capital gains when the shares are sold.

Common strategies include exercising early to start the long-term capital gains holding period sooner, spreading ISO exercises across multiple years to stay below the AMT threshold, or using a cashless exercise to reduce upfront costs. The right strategy depends on your company’s valuation, your income, and your risk tolerance. As always you should speak to your tax professional for your particular circumstance.